��˹�������Ʊ������ҵ������ǰ������

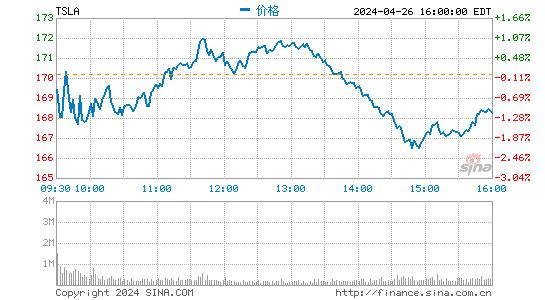

�������˲ƾ�Ѷ ����ʱ��8��8��������Ϣ����˹������(TSLA)�ܶ��������˼���������ҵ�����ִﵽ�����Ԥ�ڣ�Ͷ���߶Դ����Գ�ֿ϶����ƶ���˹���Ĺ�Ʊ���ܶ��̺����12%��������ϸ�µع۲�һ����˹�������²Ʊ���

��������ΪӢ��ԭ�Ľ��룬����Ӣ�İ汾����Ͷ���߲ο���

������˹���ļ�Ӫ��Ϊ4.01����Ԫ������ǰһ���ȵ�5.55����Ԫ��Ӧע����ǣ���˹����������Ŀӵ��1.46����Ԫ����Ӫ�գ����������һ���֣���˹����Ӫ�ս��������5.48����Ԫ��

���������GAAP(����ͨ�û����)��������֣���˹���IJƱ����á������S���͵�1934����Ԫ����ë������˹����ë������1����Ԫ����1.2����Ԫ�������ƹ�Ʊн�꣬��˹��ë��Ϊ1.2089����Ԫ��������ˣ������ƹ�Ʊн�����ǰ������Դ���Ĵ����˹����ӯ��2628����Ԫ�������˹��ÿ�ɾ�����Ϊ20���֣�����ǰһ�Ƽ���12���֣�����������ͬ�ڵ�ÿ�ɿ���89���֡�

������Ϊ��Ҫ���ǣ���˹����������ʱ���ڵ�ǰ�����˹��衣��˹��Ԥ�ƽ���������ٶȣ���ijЩ��������ŷ�ޡ�Ԥ��ŷ���г����۵�����ë���ʸ��ߣ���˹��Ԥ��85ǧ��ʱ�������������ʢ����Ӧ������ά����˹���ĸ�ë���ʡ�ŷ���г��ļ��룬��˹��������ƽ���ۼ�Ӧ�û����ǣ�������Ϊ����ŷ����Դ�ɱ��ȱ���Ҫ�ߣ����ܳ���ŷ���������������۸�

������˹��Ԥ�Ʊ����Ƚ������Գ���5ǧ����S�ͳ�������2013���ȫ��Χ�ڽ�����2.1��������˹��Ԥ��S�ͳ��������ʽ����ǣ���ZEV(���ŷ�����)����Ӫ�ս��½���Ԥ���⽫������һ����ë������20-23%֮�䡣�������ʱ����˹������ZEV�Ŵ���ë����Ӧ��ﵽ25%������ɹ�˾��ǰ������Ԥ��Ŀ�ꡣ

������˹��Ԥ��δ�����������ֽ�����Ϊ�������Ͷ������˵��һ������Ϣ����˹���������������������˾���κ�ҵ������û�б�����ֵ�ù�ע�����⣬��˹��������������г��������ǿ����2014�������۳�4�������ϵ�������

�����ܵ���˵����˹���չ�ȥ�IJƼ����ֲ������������δ���dz��ֹۡ���˹������������ء������з�Ͷ�ʺ��������Ŷ�������ο����һ���棬�ֵĽ��ں������ڳɹ����ڵ�ǰ�ɼ��еõ����֡����ǣ��Ⲣ����ζ����ֻ��Ʊ�����һ�����ǡ���˹��ӵ�кܶ������ĵ�Ͷ���ߣ���ͷ����Ҳ�ϸߡ�Ŀǰ�������¸ù��µ����ƶ����ز�̫�࣬��Ϊ��Ҫ�������һ��ͷ���ܵ��¸ù��µ��������������ѳ��ۣ�������ͷ�ѽ��֡�δ��������������˹�����δ�ȥ�����������ƽ���η�չ���˹�ע���ҹ�ע��һ���������������ɵ���������Ϊһ���г���־������µ���ǰ������ǿ���Ĺ�Ʊ��������������֮һ��δ���������У�Ͷ����˹���ƺ������Ķġ�(����/����)

����Tesla: Another Good Quarter, Encouraging Outlook

����On Tuesday evening, Tesla (TSLA) announced its quarterly earnings, and most of the company's figures were either in-line or better than expectations. Investors cheered by buying up more shares of the company, driving the share price up by as much as 12% in the after-hours. Let's take a look at Tesla's last quarter��

����The company generated $401 million in revenues, up from $22 million generated in the same quarter last year, but down from the $555 million generated in the previous quarter. Keep in mind that Tesla has $146 million in deferred revenues due to its lease program and when we include this number, the revenues jump to $548 million. The gross profit in the quarter was $100.48 million, indicating a gross margin of 24.69% not excluding the ZEV credits. The company posted an operating loss of $11.79 million due to itemized expenditures of $52 million in research and development and $60 million in selling, general and administrative (these expenses include $19.26 million of stock-based-compensations)��

����For the quarter, Tesla reported a net loss of $30.5 million. The company reported a negative cash flow of $38.19 million in operations, $27.17 million in investing activities and it generated $597 million from financial activities such as the secondary public offering it held during the quarter. As a result, Tesla currently has $749 million in cash and $578 million in long term debt��

����In non-GAAP financials, we are looking at a nicer picture. If we include the $19.34 million of deferred gross profit due to leasing of Model S, the company's gross profit jumps from $100 million to $120 million. Excluding stock based compensations, the company's gross profit was $120.89 million for the quarter. Furthermore, excluding stock based compensations and the early extinguishment of the Department of Energy loans, the company posted a net profit of $26.28 million. Finally, the company's net income per share was 20 cents, up from 12 cents in the last quarter and a loss of 89 cents in the same quarter a year ago��

����More importantly, Tesla's outlook for the rest of the year was pretty encouraging. The company expects to increase its production rate further and move some cars to Europe to sell them there. European cars are expected to have higher margins and the company expects a strong demand for its 85 kWh cars, which should keep the margins high. With the addition of European markets, the average sale price should go higher because energy-efficient cars tend to sell for higher prices in Europe due to higher energy costs in the continent compared to North America. Tesla expects to deliver a little more than 5,000 Model S cars this quarter and 21,000 cars globally by the end of 2013. Moving forward, the company expects higher margins on the cars sold but lower ZEV credit revenue, which should move its gross margin to 20-23% range for the next quarter. Towards the end of the year, the gross margins excluding ZEV credits should reach 25%�� which is in-line with the previously announced target of the company��

����The company expects to spend additional capital on growth measures, such as the purchase of additional land that was announced last month, increased research and development expenses, new retail stores, service centers and Supercharger locations. These are one-time investments that should pay themselves off in the following years as long as the company is profitable. The next 2 quarters, the company expects to be cash flow positive which is nice to hear. The company announced a "growing demand" without specifying any numbers which is interesting. On the other hand, the company announced that it could sell more than 40,000 cars in 2014 if the demand continues to be strong in the international markets��

����Tesla generally had a decent quarter and the management seems very optimistic about the future. I like the fact that it is buying additional land, ramping up research and development investments and getting serious about expanding. On the other hand, most of the short and medium term success is already priced in by the investors. Of course, this doesn't mean that the stock price can't go up further. Tesla has a lot of faithful investors and a high rate of short interest. At this point, there don't seem to be many catalysts to the downside because it takes a large number of sellers or shorters to bring a company's share price down, and most sellers already sold and most shorters already shorted at this point. It will be interesting to see where Tesla goes and how the story develops in the following quarters. One thing I would watch out for is tapering of the quantitative easing because when the market goes down strongly based on fear, the high-flyers are first ones to suffer. For the next few months, Tesla doesn't sound like a bad bet��

���������˲ƾ��ɰɡ�����

�������ĵ��˻�����

- ����õĵ�Ӱ�����е�Ӱ

- ��¼�����ȵ㣺�������

- ���������ɹ����ݿ�����

- ���۾������£���������

- ����������Ϸ����������

- ���˶�ϲ���ɵģ���ɻ�

- ��ʬ���³�����ʬ��ż

- �Ѷ�����ѣ��������ֻ�

- ���Կ���Ȥζ����������

- �������е��㣺���ι���

- ���ֺ���������ѣ�����

- �����ȱȿ�����������

- ������ָ�⣺��ɫ���

- Ȧ���������������ս

- ð�ս���������տ������

- ������Ϸ������������