来源:经济学家圈

当地时间2024年9月18日,美国华盛顿特区,美联储主席鲍威尔举行新闻发布会。本文来源:澎湃新闻、华尔街见闻、新浪财经、钟正生经济分析、中金点睛、玉渊谭天。

美联储降息声明全文

北京时间9月19日凌晨,美联储发布9月议息声明,将联邦基金利率的目标区间下调50个基点至4.75%-5%,为4年来的首次降息。

美联储上一次降息还是在2020年3月,为应对新冠疫情降息1个百分点至0-0.25%。2022年3月以来,美联储启动了一轮近乎史无前例的激进加息,并从2023年7月起将政策利率维持在5.25%-5.5%高位至今。

美联储在9月的声明中表示,在考虑进一步调整联邦基金利率目标区间时,委员会将仔细评估未来数据、不断演变的前景以及风险平衡情况。美联储表示,委员会坚定地致力于支持最大限度的就业,以及将通胀恢复至2%这一目标。

声明表示,最近的指标表明,经济活动继续稳步扩张。就业增长有所放缓,失业率有所上升,但仍然保持低位。通货膨胀率朝着委员会设定的2%的目标取得了进一步进展,但仍保持一定程度的高企。

声明还提到,委员会对通胀正可持续地朝着2%迈进有了更大的信心,并判断实现就业和通胀目标的风险大致是平衡的。经济前景是不确定的,委员会对其双重任务双方的风险都很关注。此前7月的表述为“实现就业和通胀目标的风险继续趋于更好的平衡”。

声明再次提到,在评估合适的货币政策立场时,委员会将继续监测新信息对经济前景的影响。如果出现可能阻碍委员会实现目标的风险,委员会将适当调整货币政策立场。委员会的评估将考虑到大量信息,包括劳动力市场指标、通胀压力和通胀预期指标、金融和国际形势发展的数据等。

值得一提的是,此次议息决议未能全票通过,美联储理事Michelle W. Bowman投了反对票,他倾向于降息25个基点。

以下是9月声明全文及与7月声明的比较:

最近的指标表明,经济活动继续稳步扩张。就业增长有所放缓(slowed)[7月原文:就业增长趋于温和(moderated)],失业率有所上升,但仍然保持低位。通货膨胀率朝着委员会设定的2%的目标取得了进一步进展,但仍保持一定程度的高企(7月原文为:通货膨胀在过去一年有所缓解,但仍保持一定程度的高企。最近几个月,在实现委员会2%的通胀目标方面取得了进一步进展)。

委员会力图在长期内达成最大就业和2%的通胀目标。委员会对通胀正可持续地朝着2%迈进有了更大的信心,并判断实现就业和通胀目标的风险大致是平衡的(7月原文为:委员会认为,实现就业和通胀目标的风险继续趋于更好的平衡)。经济前景不确定,委员会注意到其双重任务面临的双面风险。

考虑到通胀的进展和风险的平衡,委员会决定将联邦基金利率的目标区间下调50个基点至4.75%-5%(7月原文:为了支持其目标,委员会决定将联邦基金利率的目标区间维持在5.25%-5.5%)。在考虑对联邦基金利率目标区间进一步(7月原文:任何)调整时,委员会将仔细评估未来的数据、不断变化的前景和风险平衡。(删去7月表述:委员会认为,在对通胀持续向2%迈进有更大信心之前,降低目标区间是不合适的)。委员会将继续减持美国国债、机构债券和机构抵押贷款支持证券。委员会坚定地致力于支持最大限度的就业,以及将通胀恢复至2%这一目标(7月原文:委员会坚定致力于将通胀率恢复至2%这一目标)。

在评估合适的货币政策立场时,委员会将继续监控未来的经济数据的影响。如果风险的发生会阻碍达成委员会的双重目标,委员会会为调整适当的货币政策立场做好准备。委员会的评估将考虑到大量信息,包括劳动力市场指标、通胀压力和通胀预期指标、金融和国际形势发展的数据等。

投票赞成者包括:FOMC委员会主席(美联储主席)鲍威尔(Jerome H. Powell, Chairman);委员会副主席(纽约联储主席)威廉姆斯(John C. Williams,Vice Chairman);(里士满联储主席)Thomas I. Barkin;(美联储理事)Michael S. Barr;(亚特兰大联储主席)Raphael W. Bostic; (删去:美联储理事Michelle W. Bowman);(美联储理事)Lisa D. Cook;(旧金山联储主席)Mary C. Daly;Beth M. Hammack(本月新增);(删去:芝加哥联储主席Austan D. Goolsbee); (美联储理事)Philip N. Jefferson;(美联储理事)Adriana D. Kugler;(美联储理事)Christopher J. Waller。投票反对这一行动的有(美联储理事)Michelle W. Bowman,他倾向于将联邦基金利率的目标区间下调25个基点。■

鲍威尔发布会

回答媒体提问前的讲稿全文

9月18日周三,美联储主席鲍威尔的记者会回答媒体提问前的讲稿全文(中英对照)

Good afternoon, my colleagues and I remain squarely focused on achieving our dual mandate goals of maximum employment and stable prices for the benefit of the American people.

下午好,我和我的同事们仍然专注于实现美联储的双重目标,即最大化就业和稳定物价,以造福美国人民。

Our economy is strong overall and has made significant progress toward our goals. Over the past two years, the labor market has cooled from its formerly overheated state. Inflation has eased substantially from a peak of 7% to an estimated 2.2% as of August, we‘re committed to maintaining our economy’s strength by supporting maximum employment and returning inflation to our 2% goal.

美国经济总体强劲,并已朝着我们的目标取得了重大进展。在过去两年中,劳动力市场已从之前的过热状态降温。截至8月,通货膨胀率已从7%的峰值大幅下降至8月份估计的2.2%。美联储致力于通过支持最大化就业和将通胀率恢复到2%的目标来保持经济强劲。

Today, the Federal Open Market Committee decided to reduce the degree of policy restraint by lowering our policy interest rate by a half percentage point. This decision reflects our growing confidence that with an appropriate recalibration of our policy stance, strength in the labor market can be maintained in a context of moderate growth and inflation moving sustainably down to 2%. We also decided to continue to reduce our securities holdings. I will have more to say about monetary policy after briefly reviewing economic developments.

今天,联邦公开市场委员会决定降低政策约束程度,将政策利率下调50个基点。这一决定反映出我们越来越有信心,只要适当校准我们的政策立场,劳动力市场的强劲势头就能在温和经济增长和(5.448, 0.00, 0.00%)通胀持续下降至2%的背景下保持下去。我们还决定继续缩表。在简要回顾经济发展情况后,我将就货币政策发表更多看法。

Recent indicators suggest that economic activity has continued to expand at a solid pace. GDP rose at an annual rate of 2.2% in the first half of the year, and available data point to a roughly similar pace of growth this quarter. Growth of consumer spending has remained resilient, and investment in equipment and intangibles has picked up from its anemic pace last year. In the housing sector, investment fell back in the second quarter after rising strongly in the first. Improving supply conditions have supported resilient demand in the strong performance of the US economy over the past year. In our summary of economic projections, Committee participants generally expect GDP growth to remain solid, with a median projection of 2% over the next few years.

最近的指标显示,美国经济活动继续稳步增长。今年上半年,GDP以2.2%的年率增长,现有数据显示三季度的增长速度大致相同。消费支出增长保持韧性,设备和无形资产投资已从去年的疲软速度回升。在住房领域,投资在第一季度强劲增长后在第二季度回落。供应条件的改善支撑了美国经济在过去一年强劲表现中的韧性需求侧。在我们的经济预测摘要中,FOMC委员会参与者普遍预计美国GDP增长将保持稳健,未来几年的预测中值为2%。

In the labor market, conditions have continued to cool. Payroll job gains averaged 116,000 per month over the past three months, a notable step down from the pace seen earlier in the year. The unemployment rate has moved up, but remains low at 4.2%. Nominal wage growth has eased over the past year, and the jobs to workers gap has narrowed overall. A broad set of indicators suggest that conditions in the labor market are now less tight than just before the pandemic in 2019. The labor market is not a source of elevated in inflationary pressures. The median projection for the unemployment rate in the SEP is 4.4% at the end of this year, four tenths higher than projected in June.

劳动力市场情况持续降温。过去三个月,非农就业岗位平均每月增加11.6万个,与今年早些时候的速度相比明显放缓。失业率有所上升,但仍保持在4.2%的低位。名义工资增长在过去一年有所放缓,职位空缺与求职人数之间的差距总体上有所缩小。一系列指标表明,劳动力市场的紧张状况目前比2019年疫情爆发前有所缓解。劳动力市场并不是通胀压力高企的根源了。美联储经济预测中对今年年底的失业率中值预测为4.4%,比6月份的预测高出0.4个百分点。

Inflation has eased notably over the past two years, but remains above our longer run goal of 2%. Estimates based on the consumer price index and other data indicate that total PCE prices rose 2.2% over the 12 months, ending in August, and that excluding the volatile food and energy categories, core PCE prices rose 2.7%. Longer term inflation expectations appear to remain well anchored, as reflected in a broad range of surveys of households, businesses and forecasters, as well as measures from financial markets. The median projection in the SEP for total PCE inflation is 2.3% this year and 2.1% next year, somewhat lower than projected in June. Thereafter. The median projection is 2%.

过去两年通胀率明显下降,但仍高于我们2%的长期目标。根据消费者价格指数和其他数据估计,截至8月的12个月内,名义PCE价格将上涨2.2%,不包括波动较大的食品和能源类别,核心PCE价格将上涨2.7%。长期通胀预期似乎仍良好锚定,这反映在对家庭、企业和预测者的广泛调查以及金融市场的指标中。美联储经济预测中对今年PCE总通胀率的预测中值为2.3%,明年为2.1%,略低于6月份的预测。2026年及以后的预测中值为2%。

Our monetary policy actions are guided by our dual mandate to promote maximum employment and stable prices for the American people. For much of the past three years, inflation ran well above our 2% goal, and labor market conditions were extremely tight. Our primary focus had been on bringing down inflation, and appropriately so, we are acutely aware that high inflation imposes significant hardship as it erodes purchasing power, especially for those least able to meet the higher costs of essentials like food, housing and transportation. Our restrictive monetary policy has helped restore the balance between aggregate supply and demand, easing inflationary pressures and ensuring that inflation expectations remain well anchored.

我们的货币政策行动以促进美国人民充分就业和物价稳定为双重使命。在过去三年的大部分时间里,通货膨胀率远高于我们2%的目标,劳动力市场状况极其紧张。当时我们的主要重点是降低通胀率,这也是理所应当的,我们敏锐地意识到高通胀会造成重大困难,因为它会侵蚀购买力,尤其是对于那些最无力承担食品、住房和交通等必需品高成本的人来说。我们的限制性货币政策有助于恢复总供给和总需求之间的平衡,缓解通胀压力并确保通胀预期良好锚定。

Our patient approach over the past year has paid dividends. Inflation is now much closer to our objective, and we have gained greater confidence that inflation is moving sustainably toward 2% . As inflation has declined, the labor market has cooled, the upside risks to inflation have diminished and the downside risks to employment have increased. We now see the risks to achieving our employment and inflation goals as roughly in balance, and we are attentive to the risks to both sides of our dual mandate in light of the progress on inflation in the balance of risks.

过去一年,我们耐心的策略已获得回报。通胀现在更接近我们的目标,我们更加确信通胀正持续向2%迈进。随着通胀下降,劳动力市场已经降温,通胀的上行风险减少,就业的下行风险增加。我们现在认为实现就业和通胀目标的风险大致平衡,鉴于风险平衡中通胀的进展,我们关注双重使命中各方目标面临的风险。

At today‘s meeting, the committee decided to lower the target range for the federal funds rate by a half percentage point to four and three quarters percent to 5%. This recalibration of our policy stance will help maintain the strength of the economy and the labor market, and will continue to enable further progress on inflation as we begin the process of moving toward a more neutral stance.

在今天的会议上,委员会决定将联邦基金利率目标区间下调50个基点,至4.75%到5%。这一政策立场的重新校准将有助于保持经济和劳动力市场的强劲,并将继续推动通胀进一步下降,同时我们正开始转向更中性的立场。

We are not on any preset course. We will continue to make our decisions meeting by meeting. We know that reducing policy restraint too quickly could hinder progress on inflation. At the same time, reducing restraint too slowly could unduly weaken economic activity and employment. In considering additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook and the balance of risks.

我们没有预先设定的政策路线,将继续在每次会议上做出决定。我们知道,过快减少政策限制可能会阻碍通胀降温的进展。同时,过慢减少限制可能会过度削弱经济活动和就业。在考虑对联邦基金利率目标区间进行额外调整时,委员会将仔细评估即将公布的数据、不断变化的前景和风险平衡。

In our Sep FOMC, participants wrote down their individual assessments of an ap0propriate path for the federal funds rate based on what each participant judges to be the most likely scenario going forward, if the economy evolves as expected. The median participant projects that the appropriate level of the federal funds rate will be 4.4% at the end of This year and 3.4% at the end of 2025. These median projections are lower than in June, consistent with the projections for lower inflation and higher unemployment as well as the changed balance of risks.

在我们9月份的FOMC会议上,参与官员们根据各自对未来最可能出现情况的判断,写下了他们对联邦基金利率适当路径的评估,前提是经济按预期发展。中位数预测是,联邦基金利率的适当水平在今年年底为4.4%,2025年底为3.4%。这些中位数预测低于6月份的预测,与通胀下降、失业率上升以及风险平衡变化的预测一致。

These projections, however, are not a committee plan or decision. As the economy evolves, monetary policy will adjust in order to best promote our maximum employment and price stability goals. If the economy remains solid and inflation persists, we can dial back policy restraint more slowly. If the labor market were to weaken unexpectedly, or inflation were to fall more quickly than anticipated, we are prepared to respond.

然而,这些预测并非委员会的计划或决定。随着经济的发展,货币政策将进行调整,以最好地促进我们的最大化就业和价格稳定目标。如果经济保持稳健且通胀持续存在,我们可以更缓慢地放松政策限制。如果劳动力市场意外走弱,或者通胀下降速度快于预期,我们也准备好做出回应。

Policy is well positioned to deal with the risks and uncertainties that we face in pursuing both sides of our dual mandate. The Fed has been assigned two goals for monetary policy, maximum employment and stable prices. We remain committed to supporting maximum employment, bringing inflation back down to our 2% goal, and keeping longer term inflation expectations well anchored. Our success in delivering on these goals matters to all Americans. We understand that our actions affect communities, families and businesses across the country. Everything we do is in service to our public mission. We at the Fed will do everything we can to achieve our maximum employment and price stability goals.

政策已准备好应对我们在履行双重使命时面临的风险和不确定性。美联储被赋予了两个货币政策目标:最大化就业和稳定物价。我们仍致力于支持充分就业,将通胀率降至2%的目标,并保持长期通胀预期良好锚定。我们能否成功实现这些目标对所有美国人来说都至关重要。我们明白,我们的行动会影响全美的社区、家庭和企业。我们所做的一切都是为了履行我们的公共使命。美联储将竭尽全力实现最大化就业和物价稳定的目标。

鲍威尔9月FOMC大幅降息后

记者会问答环节

来源:华尔街见闻

问题1:Strong third quarter GDP running 3% so what changed to made the committee go 50. Andhow do you respond to the concerns that perhaps it shows the Fed is more concerned about the labor market, and I guess should we expect more 50s in the months ahead? And based on what should we make that call?

第三季度美国GDP预计强劲增长3%,那么是什么变化让美联储决定降息50个基点?这是否可能表明美联储更担心劳动力市场,未来也会继续每次降息50个基点?我们应该根据什么做出这一判断?

回答1:Let me jump in. So since the last meeting, we have had a lot of data come in. We‘ve had the two employment reports July and August. We’ve also had two inflation reports, including one that came in during blackout. We had the QCW report, which suggests that the payroll report numbers that we‘re getting may be artificially high and will be revised down. You know that we’ve also seen that anecdotal data like the Beige Book, so we took all of those, and we went into blackout, and we thought about what to do, and we cleared that this was the right thing for the economy, for the people that we serve, and that‘s how we made our decision. So that’s one question.

自上次会议以来,我们收到了很多数据,有7月和8月的两份非农就业报告,还有两份通胀报告,其中一份是在美联储官员静默期内发布的。还有QCW报告表明我们非农新增就业数可能被人为抬高,将会被下调。我们也看到了像美联储褐皮书这样的轶事数据,所以我们收集了所有这些数据,然后进入公开发言的静默期,我们思考该怎么做,并明确了这对经济、对我们服务的美国人民来说是正确的,这就是我们做出决定的方式。

So a couple things, a good place to start is the SEP. But let me start with what I said, which was that we‘re going to be making decisions, meeting by meeting, based on the incoming data, the evolving outlook, the balance of risks. If you look at the SEP, you’ll see that it‘s a process of recalibrating our policy stance, away from where we had a year ago, when inflation was high and unemployment low, to a place that’s more appropriate given where we are now and where we expect to be. And that process will take place over time. There‘s nothing in the SEP that suggests the committee is in a rush to get this done. This this process evolves over time.

(对于未来利率路径的判断),一个好的起点是看经济预测摘要SEP。首先,我们将根据收到的数据、不断变化的前景和风险平衡,在逐次会议上做出决定。看看 SEP你会发现,这是一个重新校准我们政策立场的过程,远离一年前通胀高+失业率低的立场,转向一个更适合当前情况和我们预期的立场。这个过程将随着时间的推移而发生。SEP中没有任何内容表明委员会急于完成(降息)这项工作,这个过程是随着时间的推移而发展的。

Of course, that‘s a projection. That’s a baseline projection. We know, as I mentioned in my remarks, that the actual things that we do will depend on the way the economy evolves. We can go quicker, if that‘s appropriate, we can go slower if that’s appropriate. We can pause if that‘s appropriate. But that’s what we‘re contemplating. Again, I would point you to the SEP as just an assessment of where, what the committee is thinking today, but the individual members, rather, of the committee, are thinking today, assuming that their particular forecasts take, you know, are realized.

当然,这只是一个预测。这是一个基线预测。正如我在发言中提到的,我们实际做的事情将取决于经济的发展方式。如果合适,我们可以加快(降息)速度,如果合适,我们可以放慢速度。如果合适,我们可以暂停。但这就是我们正在考虑的。再次,我想指出,SEP只是对委员会今天的想法的评估,而且是委员会的各位成员今天的想法,假设他们特定的预测得以实现。

问题2: The projections show that the Fed officials expect the Fed funds rate to still be above their estimate of long run neutral by the end of next year. So does that suggest you see rates as restrictive for that entire period? Does that threaten the weakening of the job market you said you‘d like to avoid, or does it suggest that maybe people see the short run neutral as a little bit higher?

预测显示,美联储官员预计到明年年底联邦基金利率仍将高于他们对长期中性利率的估计。那么这是否意味着您认为利率在整个时期内都是有限制性的?这是否威胁到您所说希望避免的就业市场疲软,是否也意味着人们可能认为短期中性利率会略高一些?

回答2:I would really characterize it as this. I think people write down their estimate. Individuals do. I think every single person on the committee, if you ask them, what‘s your level of certainty around that, and they would say there’s a wide range where that could fall. So I think we don‘t know there are model based approaches and empirically based approaches that estimate what the neutral rate will be at any given time. But realistically, we know it by its works. So that leaves us in a place where we’ll be, where we expect, in the base case, to be continuing to remove restriction, and we‘ll be looking at the way the economy reacts to that, and that will be guiding us in our thinking about the question that we’re asking at every meeting, which is, is our policy stance the appropriate one?

我真的会这样描述它。这是委员会每个官员个人的预估值,如果你问他们对此的确定程度如何,他们会说,这个范围可能很大。所以我认为我们不知道是否有基于模型的方法和基于经验的方法可以估计任何给定时间的中性利率。但实际上,我们通过它的工作原理来了解它。因此,在基本场景下,我们预计会继续放松货币政策,我们将关注经济对此的反应,这将指导我们思考在每次会议上提出的问题,即我们的政策立场是否合适?

We know, if you go back, we know that the policy stance we adopted in July of 2023 came at a time when unemployment was three and a half percent and inflation was 4.2%. Today, unemployment is up to 4.2%, inflation is down to a few tenths above 2%, so we know that it is time to recalibrate our policy to Something that is more appropriate given the progress on inflation and on employment moving to a more sustainable level. So the balance of risks are now even, and this is the beginning of that process I mentioned, the direction of which is toward a sense of neutral, and we‘ll move as fast or as slow as we think is appropriate in real time, what you have is our individual accumulation of individual estimates of what that will be in the base case.

我们知道,如果回顾一下,我们会发现在2023年7月采取的政策立场是在失业率为3.5%和通胀率为 4.2%时采取的。如今,失业率已升至 4.2%,通胀率降至更接近2%,因此我们知道,鉴于通胀和就业向更可持续水平迈进的进展,现在是时候重新调整我们的政策,使其更合适。因此,风险平衡现在已均衡,这是我提到的那个过程的开始,其方向是朝着中立的方向发展,我们将根据我们认为对当时合适的速度或快或慢地采取行动,点阵图是联储官员对基本场景的个人估计值。

问题3:How close was this in terms of the decision, you do have the first dissent by a governor since 2005 I think was the weight clearly in favor of a 50, or was this a very close decision?

这是自 2005 年以来第一次有联储理事提出异议,降息50个基点的共识意见有多少?

回答3:I think we had a good discussion. You know, if you go back, I talked about this at Jackson Hole, but I didn‘t address the question of the size of the cut. And I think we left it open going into blackout. And so there was a lot of discussion back and forth. Good diversity of division. Excellent discussion today. I think there was also broad support for the decision that the committee voted on. So I would add, though, look at the SEP all 19 of the participants wrote down multiple cuts this year, all 19. That’s a big change from June, right? 17 of the 19 wrote down three or more cuts, and 10 of the 19 wrote down four more cuts. So, you know, there is a dissent, and there‘s a range of views, but there’s actually a lot of common ground as well.

我认为我们进行了很好的讨论。我在杰克逊霍尔谈到了这个问题,但我没有回答降息幅度的问题。我认为我们在静默期之前没有解决这个问题。因此,我们进行了大量的讨论。观点有多样性很好。今天的讨论非常精彩。我认为委员会投票通过的决定也得到了广泛的支持。我想补充一点,看看 SEP,所有19名参与者支持今年多次降息,这与6月份相比有很大变化,19人中有17人支持今年降息3 次或更多,有10人支持4次以上的降息。所以,存在不同意见,也有各种观点,但实际上也有很多共同点。

问题4: on the pacing here, would you expect this to be running every other meeting?

按照这样的节奏,您是否认为每隔一次会议都会进行这样(大幅降息)的讨论?

回答4:Once we get into next year, we‘re going to take it meeting by meeting, as I mentioned, we would. There’s no sense that the committee feels it‘s in a rush to do this. We made a good, strong start to this. And that’s really, frankly, a sign of our confidence, confidence in inflation is coming down toward 2% on a sustainable basis. That gives us the ability we can, you know, make a good, strong start. But, and I‘m very pleased that we did to me the logic of this, both from an economic standpoint and also from a risk management standpoint, was clear, but I think we’re going to go carefully meeting by meeting and make our decisions as we go.

一旦进入明年,我们将逐次会议讨论此事,正如我之前提到的那样。委员会不会急于这样做(降降息)。我们已经取得了良好的开端。坦率地说,这确实表明了我们的信心,相信通胀率将以可持续的方式下降到 2%。这让我们有能力取得良好的开端。但是,我很高兴我们做到了,无论是从经济角度还是从风险管理角度来看,这其中的逻辑都很明确,但我认为我们将在每次会议上都谨慎行事,并随着时间推进做出决定。

问题5:Your colleagues in your economic projections today see the unemployment rate climbing to 4.4% and staying there, obviously, historically, when the unemployment rate climbs that much over a relatively short period of time, it doesn‘t typically just stop. It continues increasing. And so I wonder if you can walk us through why you see the labor market stabilizing sort of, what’s the mechanism there, and what do you see as the risks?

您的同事在今天的经济预测中预测失业率将攀升至4.4%并保持在这个水平,显然,从历史上看,当失业率在相对较短的时间内攀升到这个水平时,它通常不会停止,而是会继续上升。所以为什么您认为劳动力市场会趋于稳定,其中的机制是什么,您认为存在哪些风险?

回答5:So again, the labor market is actually in solid condition, and our intention with our policy move today is to keep it there. You can say that about the whole economy. The US economy is in good shape. It‘s growing at a solid pace. Inflation is coming down. The labor market is in a strong pace. We want to keep it there that’s what we‘re doing.

所以,劳动力市场实际上处于稳健状态,我们今天采取政策举措的目的是保持这种状态。你可以说整个经济都是如此。美国经济状况良好。它正以稳健的速度增,通胀正在下降,劳动力市场发展强劲。我们希望保持这种状态,这就是我们正在做的事情。

问题6:“新美联储通讯社”Nick Timiraos的提问,鉴于近期就业数据的大幅修正,今天的行动是否构成追赶,或者这次比典型降息幅度更大的降息是政策利率名义水平上升的结果,因此可以预期加速降息的节奏将继续下去?

回答6:multiple questions in every list. So I would say we don‘t think we’re behind. We do not think we‘re. We think this is timely, but I think you can take this as a sign of our commitment not to get behind. So it’s a strong move.

我们不认为我们落后(于曲线)了。我们认为这是及时的(降息),但我认为你可以把这看作是我们承诺不落后(于曲线)的标志。所以这是一个强有力的举措。

I think it‘s about we come into this with a policy position that was put in place. As you know, I mentioned in July of 2023 which was a time of high inflation and very low unemployment, we’ve been very patient about reducing the policy rate. We‘ve waited. Other central banks around the world have cut many of them several times. We’ve waited, and I think that that patience has really paid dividends in the form of our confidence that inflation is moving sustainably under 2% so I think that is what enables us to take this strong move today.

我认为,关键在于我们以既定的政策立场来应对这一问题。如你所知,我提到,2023年7月是高通胀和低失业率时期,我们一直非常耐心地等待降低政策利率的时机。我们一直在等待。世界各地的其他央行已经多次降息,但美联储一直在等待,我认为这种耐心确实带来了回报,我们有信心通胀率将持续低于 2%,所以我认为这就是我们今天能够采取这一有力举措的原因。

I do not think that anyone should look at this and say, Oh, this is the new pace. You know, you have to think about it in terms of the base case. Of course, what happens will happen. So in the base case, what you see is, look at the SEP you see cuts moving along. The sense of this is we‘re recalibrating policy down over time to a more neutral level, and we’re moving at the pace that we think is appropriate given developments in the economy. And the base case, the economy can develop in a way that would cause us to go faster or slower, but that‘s what the base case says.

我认为,任何人都不应该看到这一点就说,哦,(降息50个基点)这是新的节奏。你知道,你必须从基本场景的角度来考虑。当然,该发生的事总会发生。所以在基本情况下,你看到的是,看看 SEP,你会看到降息在进行。这意味着我们正在随着时间的推移将政策重新调整到更中性的水平,我们正在以我们认为适合经济发展的步伐前进。在基本场景下,经济发展的方式可能会导致我们走得更快或更慢,但这就是基本场景所说的。

问题7: If I could follow up on the balance sheet in 2019 when you did the mid cycle adjustment, you ceased the balance sheet runoff with a larger cut. Today, is there any should there be any signal inferred about how the committee would approach end state on the balance sheet policy?

有关2019年的资产负债表,当时您进行了中期周期调整,停止了资产负债表缩减,并进行了更大的降息。今天,是否有任何信号可以推断委员会将如何处理资产负债表政策的最终状态?

回答7:So in the current situation, reserves have really been stable. They haven‘t come down. So reserves are still abundant and expected to remain so for some time. As you know, the shrinkage in our balance sheet has really come out of the overnight. RFP, so I think what that tells you is we’re not thinking about stopping runoff because of this at all. We know that these two things can happen side by side, in a sense, they‘re both a form of normalization. And so for a time, you can have the balance sheet shrink, you would also be cutting rates.

因此,在当前情况下,银行储备金确实很稳定。它们没有下降。因此储备金仍然充足,预计还会持续一段时间。如您所知,我们的资产负债表的缩减确实是一夜之间发生的。我们根本没有考虑会停止缩表。我们知道这两件事(降息+缩表)可以同时发生,从某种意义上说,它们都是一种正常化形式。因此,在一段时间内,您可以缩减资产负债表,同时还可以降低利率。

问题8: just following up on rising unemployment, is it your view that this is just a function of a normalizing labor market? amid improved supply, or is there anything to suggest that something more concerning, perhaps is taking place here given that other metrics of labor demand have softened. is do you not? Why should we not expect a further deterioration in labor market conditions if policy is still restricted?

跟进失业率上升的问题,您是否认为这只是劳动力市场正常化的结果?供应增加,还是有什么迹象表明,鉴于劳动力需求的其他指标已经减弱,也许正在发生更令人担忧的事情?您不这么认为吗?如果利率政策仍然具有限制性,为什么我们不应该预期劳动力市场状况会进一步恶化?

回答8:So I think what we‘re seeing is clearly labor market conditions have cooled off by any measure, as I talked about in Jackson Hole and but they’re still at a level. The level of those conditions is actually pretty close to what I would call maximum employment, you know. So you‘re close to mandate, maybe at mandate on that. So what’s driving it? Clearly, payroll job creation has moved down over the last few months, and this bears watching, meant by many other measures, the labor market has returned to or below 2019 levels, which was a very good, strong labor market, but this is more sort of 2018、2017. So the labor market bears close watching, and we‘ll be giving it that but ultimately, we think, we believe, with an appropriate recalibration of our policy that we can continue to see the economy growing and that will support the labor market in the meantime, if you look at the growth and economic activity data, retail sales data that we just got, second quarter GDP, all of this indicates an economy that is still growing at a solid pace, So that should also support the labor market over time.

很明显,无论以何种标准衡量,劳动力市场状况都已经降温,就像我在杰克逊霍尔会议上谈到的那样,但它们仍然处于一定水平。这些条件的水平实际上非常接近我所说的充分就业。所以接近美联储的法定使命,也许已经达到法定使命了。那么是什么推动了它呢?显然,就业岗位创造在过去几个月有所下降,这值得关注,从许多其他指标来看,劳动力市场已经回到或低于 2019 年的水平,当时是一个非常好、强劲的劳动力市场,但现在更像是 2018 年、2017 年的情况。因此,劳动力市场需要密切关注,我们也会给予关注,但最终,我们相信,通过适当调整政策,我们可以继续看到经济增长,这将支持劳动力市场,与此同时,如果你看看增长和经济活动数据、我们刚刚得到的零售额数据、第二季度的GDP,所有这些都表明美国经济仍在稳步增长,因此这也应该会随着时间的推移支持劳动力市场。

So, but again we‘re watching, and just on the point about starting to see rising layoffs. If that were to happen, wouldn’t the committee already be too late in terms of avoiding a recession?

追问:所以,我们再次关注,并且正值裁员人数开始上升之际。如果发生这种情况,委员会在避免经济衰退方面是否已经太迟了?

So we‘re, that’s, you know, our plan, of course, has been to begin to recalibrate, and we‘re not seeing rising claims, we’re not seeing rising layoffs, we‘re not seeing that, and we’re not hearing that from companies that that‘s something that’s getting ready to happen. So we‘re not waiting for that because, you know, there is thinking that the time to support the labor market is when it’s strong, and not when you begin to see the White House. There‘s some more on that. So that’s the situation we‘re in. We have, in fact, begun the cutting cycle now, and we’ll be watching, and that will be one of the factors that we consider. Of course, we‘re going to look at the totality of the data as we make these decisions, meeting by meeting.

我们的计划当然是开始重新调整政策,我们没有看到失业救济申请数量上升,也没有看到裁员人数上升,也没有听到公司说这些事情即将发生。所以我们不会等待,因为,有人认为,支持劳动力市场的最佳时机是当它强劲时。关于这一点,还有更多内容。这就是我们所处的情况。事实上,我们现在已经开始了降息周期,我们会密切关注(劳动力市场降温),这将是我们考虑的因素之一。当然,在每次会议上,我们都会查看所有数据,然后做出这些决定。

问题9:what would constitute for you and the committee a deterioration in the labor market you‘re pricing in, basically, by the end of next year, 200 basis points of cuts just to maintain a higher unemployment Rate. Would you be moving to a more preemptive monetary policy style, rather than, as you did with inflation, waiting until the data gave you a signal

什么会对您和委员会构成“劳动力市场的恶化”?您认为,到明年底,降息200个基点只是为了维持较高的失业率。您会采取更具先发制人的货币政策风格吗?而不是像您在通胀问题上所做的那样,等到数据给您一个信号再行动。

回答9:we‘re going to be watching all of the data, right? So if, as I mentioned in my remarks, if the labor market were to slow unexpectedly, then we have the ability to react to that by cutting faster. We’re also going to be looking at our other mandate. Though we have greater confidence now that inflation is moving down to 2% but at the same time, our plan is that we will be at 2% over time. So and policy we think is still restrictive, so that should still be happening.

我们会关注所有数据,因此,如果劳动力市场意外放缓,我们有能力通过加快降息来应对。我们还将关注另一个通胀的使命。虽然我们现在更有信心通胀率正降到2%,但与此同时,我们的计划是随着时间的推移通胀率将达到 2%。因此,我们认为政策仍然具有限制性,因此应该仍会如此。

I‘m just curious as to how sensitive you’ll be to the labor market, since you forecast we are going to see higher unemployment, and it is going to take a significant amount of monetary easing to just maintain it.

追问:我只是好奇您对劳动力市场的敏感度如何,因为您预测我们将会看到更高的失业率,而且需要大量的货币宽松政策才能维持这种状态。

So you know what I would say is we don‘t think we need to see further losing in labor market conditions to get inflation down to 2% but we have a dual mandate. And I think you can take this, this whole action as takes take a step back. What have we been trying to achieve? We’re trying to achieve a situation where we restore price stability without the kind of painful increase in unemployment that has come sometimes with disinflation. That‘s what we’re trying to do, and I think you can take today‘s action as a sign of our strong commitment to achieve that goal.

我想说的是,我们认为我们不需要看到劳动力市场状况进一步恶化来把通胀率降至2%,但我们有双重使命。我认为你可以把这整个行动看作是退一步思考。我们一直在努力实现什么目标?我们正努力实现一种局面,即恢复价格稳定,而不会出现有时伴随通货紧缩而来的那种痛苦的失业率上升。这就是我们正在努力做的事情,我认为你可以把今天的行动看作是我们实现这一目标的坚定承诺的标志。

当地时间2024年9月18日,美国华盛顿特区,美联储主席鲍威尔举行新闻发布会。

当地时间2024年9月18日,美国华盛顿特区,美联储主席鲍威尔举行新闻发布会。问题10:You‘re describing this view that you don’t think you‘re behind when it comes to the job market. Can you walk us through the specific data points that you found to be most helpful in the discussions at this meeting? You mentioned a couple, but would you be able to walk us through what that dashboard told you as far as what you know about the job market now?

您描述了这种观点,即美联储认为自己在就业市场方面并不落后。能向我们介绍一下您认为在本次会议讨论中最有帮助的具体数据点吗?您提到了几个,当前就业市场还有哪些信息去关注?

回答10:Sure. So start with unemployment, which is the single most important one. Probably you‘re at 4.2% that’s, you know, I know that‘s higher than we were. We were used to seeing numbers in the mid and even below mid threes last year. But if you look back over the sweep of the years, that’s a low, that‘s a very healthy unemployment rate. And anything in the low fours is, A, really, is a good labor market. So that’s one thing. Participation is at high levels, it‘s, you know, we’ve had, we‘re right adjusted for demographics, for aging, participation, said, at pretty high levels, that’s a good thing. Wages are still a bit above what would be their wage increases. Rather, are still just a bit above where they would be over the very longer term to be consistent with 2% inflation, but they‘re very much coming down to what that sustainable level is. So we feel good about that. Vacancies over per unemployed is back to what is still a very strong level. It’s not as high as it was. That number reached two to one, two vacancies for every unemployed person as measured, it‘s now around one, but that’s still, that‘s still a very good number. I would say quits have come back down to normal levels. I mean, that could go on and on there.

首先是失业率,这是最重要的一个因素。失业率4.2%比去年要高,过去失业率在3%的中段或更低,如果回顾这些年,你会发现这是一个很低、非常健康的失业率。任何低于4%的失业率都表明劳动力市场状况良好。这是一方面。就业参与率处于高水平,我们已经根据人口统计学、老龄化等因素进行了调整,就业参与率处于相当高的水平,这是件好事。工资仍略高于应有的工资增长水平,更确切地说,仍略高于与2%通胀率保持一致的长期工资增长水平,但它们正在逐渐降至可持续水平。所以我们对此感到满意。每名失业人员对应的空缺职位数下降,但仍是非常强劲的水平,没有以前那么高了,以前达到二比一,即每名失业者对应两个职位空缺,现在大约是一比一,这仍是一个非常好的数字。辞职率已经回落到正常水平,这种情况可能会一直持续下去。

There are many, many employment indicators. What do they say? They say this is still a solid labor market. The question isn‘t the level. The question is that there has been change over, particularly over the last few months, and you know, so what we say is, as the upside risk to inflation have really come down, the downside risk to employment have increased , and because we have been patient and held our fire on cutting wall inflate While inflation has come down. I think we’re now in a very good position to manage the risks to both of our goals.

就业指标有很多。它们怎么说呢?它们说这仍然是一个稳固的劳动力市场。问题不在于水平。问题在于,特别是在过去几个月里,情况发生了变化,所以我们说,随着通胀的上行风险确实下降,就业的下行风险增加了,因为我们一直保持耐心,在通胀下降的同时,控制通胀。我认为我们现在处于非常有利的位置,可以管理我们两个使命各自面临的风险。

And what do you expect to learn between now and November that will help inform the scale of the cut of the next meeting?

追问:您期望从现在到 11 月之间了解到哪些信息,以协助确定下次会议的降息幅度?

You know, more data. The usual. Don‘t look for anything else. We’ll see another labor report. We‘ll see another jobs report. I think we get. We actually, we could to, we get a second jobs report on the day of the meeting. I think, no, no, on the Friday before the meeting. So and inflation data we’ll get, we‘ll get all this data we’ll be watching. You know, it‘s always a question of, look at the incoming data and ask, what are the implications of that data for the evolving outlook and the balance of risks? And then go through our process and think, what’s the right thing to do? Is policy where we want it to be, to foster the achievement of our goals over time. So that‘s what it is, and that’s what we‘ll be doing.

你知道,更多的数据。和往常一样。不要再寻找其他东西了。我们将看到两份劳动力报告,我们还将获得通胀数据,即所有这些我们将关注的数据。你知道,这总是一个问题,看看传入的数据,并问,这些数据对不断变化的前景和风险平衡有何影响?然后通过我们的流程思考,什么是正确的做法?政策是否符合我们的期望,是否有助于实现我们的目标。所以这就是我们要做的。

问题11:we‘ve only been running a little above 100,000 jobs a month on payrolls last three months. Do you view that level of job creation as worrying or alarming, or would you be would you be content if we were to kind of stick at that level? And relatedly, one of the welcome trends over the last couple of years has been labor market steam coming out through job openings, falling rather than job losses. Do you think that trend has further to run? Or do you see risk that further labor market cooling will have to come through job losses?

过去三个月,我们每月新增就业岗位仅略高于10万个。您认为这种就业岗位增加水平令人担忧或发出警报吗?或者,如果我们一直保持这种水平,您会感到满意吗?与此相关的是,过去几年中令人欣喜的趋势之一是劳动力市场热度通过职位空缺释放出来,而不是职位减少。您认为这种趋势会持续下去吗?或者,您是否认为劳动力市场进一步降温的风险将不得不通过职位减少来实现?

回答11:So on the job creation, it depends on the inflows, right? So if you‘re having millions of people come into the labor force then, and you’re creating 100,000 jobs, you‘re going to see unemployment go up. So it really depends on what’s the trend underlying the volatility of people coming into the country. We understand there‘s been quite an influx across the borders, and that has actually been one of the things that’s allowed unemployment rate to rise as and the other thing is just the slower hiring rate, which is something we also watch carefully. So it does depend on what‘s happening on the supply side and on the curve.

就业创造取决于人口流入就业市场,所以,如果有数百万人进入劳动力市场,而且只创造了10万个就业岗位,那么失业率就会上升。所以,这实际上取决于流入该国的人口波动背后的趋势。我们知道跨境移民流入量相当大,这实际上是导致失业率上升的原因之一,另一个因素是招聘速度放缓,这也是我们密切关注的因素。所以,这确实取决于供应方面和供需曲线的情况。

So we all felt on the committee, not all, but I think everyone on the committee felt that job openings were so elevated that they could fall a long way before you hit the part of the curve where job openings turned into higher unemployment, job loss. And yes, I mean, I think we are. It‘s hard to know that. You can’t know these things with great precision, but certainly it appears that we‘re very close to that point, if not at it so that further declines in job openings will translate more directly into into unemployment. But it’s been, it‘s been a great ride down. I mean, we’ve seen a lot of of tightness come out of the labor market in that form without it resulting in lower employment.

因此,我认为委员会的每个人都认为,职位空缺数量如此之高,所以可以长时间下降直到传导称更高的失业率上升。很难知道何时达到这一点。你不可能非常准确地知道这些事情,但可以肯定的是,我们非常接近那个点,甚至现在都可能就在这个点上了,那么职位空缺的进一步减少将更直接地转化为失业。但这是一个巨大的下降过程。我的意思是,我们已经看到劳动力市场以这种形式缓解了很多紧张局面,但并没有导致就业率下降。

问题12:so we‘ve heard some speculation that you may be going with the federal funds rate to three and a half, maybe under 4% and there’s basically an entire generation that has experienced zero or near zero federal fund rate as something we‘re heading in that direction. Again. What’s the likelihood that cheap money is now the norm?

我们听到一些猜测,称联邦基金利率可能会降至 3.5%,也许低于 4%,而基本上整整一代人都经历过零或接近零的联邦基金利率,我们正朝着这个方向前进。廉价货币/超低利率重新成为常态的可能性有多大?

回答12:So this is a question. You mean, after we get through all of this, it‘s just great question that we just we can only speculate about. Intuitively, most many, many people anyway, would say we’re probably not going back to that era where there were trillions of dollars of sovereign bonds trading at negative rates, long term bonds trading at negative rates. And it looked like the neutral rate was might even be negative. So there was people were issuing debt, issuing debt at negative rates. It seems that‘s so far away. Now, my own sense is that that we’re not going back to that, but you know, honestly, we‘re going to find out. But you know, it feels, it feels to me and that the neutral rate is is probably significantly higher than it was back then. How high is it? I just don’t think we know it‘s again, we only know it by its works.

我们只能对此进行推测。直觉上,大多数人会说,我们可能不会回到那个时代,当地有数万亿美元的主权债券以负利率交易,长期债券以负利率交易,而且当时看起来中性利率甚至可能为负。所以有人在以负利率发行债务。这似乎距离现在已经很遥远了。我的感觉是我们不会回到那个时代,我感觉中性利率可能比当时高得多。它有多高?我也不知道,只能通过它的工作来了解它。

One more, how do you respond to the criticism that will likely come that a deeper rate cut now before the election, has some political motivations.

追问:还有一个问题,您如何回应可能出现的批评,即在选举前大幅降息是出于某些政治动机?

Yeah, so, you know, this is my fourth presidential election at the at the Fed, and you know, it‘s always the same. We’re always, we‘re always going into this meeting in particular and asking, what’s the right thing to do for the people we serve. And we do that, and we make a decision as a group, and then we announce it, and it‘s that’s always what it is. It‘s never about anything else. Nothing else is discussed. And I would also point out that the things that we do really affect economic conditions for the most part with with a lag. So nonetheless, this is what we do. Our job is to support the economy on behalf of the American people, and if we get it right, this will benefit the American people significantly. So this really concentrates the mind, and it’s something we all take very, very seriously. We don‘t put up any other filters. I think if you start doing that, I don’t know where you stop. And so we just want to do that.

这是我在美联储第四次经历美国总统大选,你知道,总是一样。我们总是问自己,对我们服务的美国人民来说,什么是正确的事情。我们这样做,我们作为一个团体做出决定,然后我们宣布它,它总是如此。它从不涉及其他任何事情。没有其他讨论。我还要指出的是,我们所做的事情确实在很大程度上影响了经济状况,而且存在滞后效果。所以尽管如此,这就是我们的工作。我们的工作是代表美国人民支持经济,如果我们做对了,这将极大地造福美国人民。所以这真的让我们集中注意力,这是我们都非常非常重视的事情。我们没有设置任何其他过滤器。否则如果你开始这样做,我不知道你会在哪里停下来。

问题13:My first question is,very simply, what message are you trying to send American consumers, the American people with this unusually large rate cut?

我的第一个问题很简单:通过这次不同寻常的大幅降息,您想向美国消费者、美国人民传达什么信息?

回答13:I would just say that, you know, the US economy is in a good place and and our decision today is designed to keep it there. More specifically, the economy is growing at a solid pace. Inflation is coming down closer to our 2% objective over time, and the labor market is is still in solid shape. So our intention is really to maintain the strength that we currently see in the US economy, and we‘ll do that by returning rates from their high level, which has really been the purpose of which has been to get inflation under control. We’re going to move those down over time to a more normal level over time,

我只想说,美国经济状况良好,我们今天的决定旨在保持这种状况。更具体地说,经济正在稳步增长。随着时间的推移,通胀正在下降接近我们2%的目标,劳动力市场仍然状况良好。所以我们的意图实际上是保持我们目前看到的美国经济的强劲势头,我们将通过把利率从高位拉低来实现这一目标,保持利率高位的目的是控制通胀。我们将随着时间推移将利率降至更正常的水平。

just a follow up to that, listening to you talk about inflation moving meaningfully down to 2% is the Federal Reserve effectively declaring a decisive victory over inflation and rising prices.

追问:听您谈论通胀率大幅下降至2%,这实际上意味着美联储在对抗通胀和物价上涨方面取得了决定性的胜利吗?

No, we‘re not so inflation. You know what we say is we want inflation. The goal is to have inflation move down to 2% on a sustainable basis. And, you know, we’re not really, we‘re close, but we’re not really at 2% and I think we‘re going to want to see it be, you know, around 2% and close to 2% for some time, but we’re certainly not doing, we‘re not we’re not saying mission accomplished or anything like that. But I have to say, though we‘re encouraged by the progress that we have made.

不,我们不会那么担心通胀。我们想要(一定程度的)通货膨胀。目标是让通胀率可持续地降至 2%。但我们现在没有真正达到2%,可能会在一段时间内接近2%,所以我们不会说(抗击通胀的)任务已经完成了这种话。但我必须说,我们对所取得的进展感到鼓舞。

问题14:我只是想知道委员会如何看待我们所看到的持续的住房通胀,您认为住房通胀率这么高,整体通胀能回到2%目标吗?

回答14:Yeah, so housing inflation is the is the one piece that is kind of dragging a bit. If I can say we know that market rents are doing what we would want them to do, which is to be moving up at relatively low levels, but they‘re not rolling over that the leases that are rolling over are not coming down as much, and OER is coming in high. So, you know, it’s been slower than we expected. I think we now understand that it‘s going to take some time for those lower market rents to get into this. But, you know, the direction of travel is clear, and as long as market rents remain, you know, relatively low inflation over time that will show up just the time it’s taking now, several years, rather than just one or two cycles of of annual lease renewals. So that‘s, I think we understand that now, I don’t think the outcome is in doubt again. As long as market rents remain under control, the outcome is not as in doubt. So I would say it‘s the rest of the rest of the portfolio, of the elements that go into core, PCE, inflation or have behaved pretty well. You know, they’re all they all have some volatility. We will get down to 2% inflation, I believe, and I believe that ultimately, we‘ll get what we need to get out of the housing services piece too, some of your colleagues have experienced concern.

是的,住房通胀是一个有点拖累的因素。不过现在市场租金正在做我们希望它们做的事情,即在相对较低的水平增长,但是续约房屋的租金并没有下降那么多,而OER却很高。所以,住房通胀降温的速度比我们预期要慢。我认为我们现在明白,那些较低的市场租金需要一段时间才能发挥作用。但是,前进的方向是明确的,只要市场租金保持相对较低的通胀,随着时间推移,拉低通胀的效果就会显现出来,这需要几年,而不仅仅是一两个年度租约续签周期。所以,我不会因此质疑通胀降温。只要市场租金保持受控,结果就不会有疑问,另外,经济数据的其他部分,包括核心PCE通胀等表现都相当不错。你知道,它们都有一定的波动性。我相信,我们的通胀率会降到 2%,我相信,最终,我们也会从住房服务部分获得所需的收益。

It‘s hard to gain that out. The housing market is in part frozen because of lock in with low rates. People don’t want to sell their homes, so because they have a very low mortgage to be quite expensive to refinance. As rates come down, people will start to move more, and that‘s probably beginning to happen already. But remember, when that happens, you’ve got a you‘ve got a seller, but you’ve also got a new buyer, in many cases. So it‘s not, you know, obvious how much additional demand that would make me the real issue with housing is that we have had and are on track to continue to have not enough housing. And so it’s going to be challenging. It‘s hard to find to zone lots that are in places where people want to live. It’s all of the aspects of housing are more and more difficult. And you know, where are we going to get the supply? And this is not something that the Fed can can really fix, but I think as we normalize rates, you‘ll see the housing market normalize. And I mean ultimately, by getting inflation broadly down and getting those rates normalized and getting the housing housing cycle normalized, that’s the best thing we can do for householders. And then the supply question will have to be dealt with by the market and also by government.

甚至,你知道,这种情况发生的可能性有多大?你会如何应对房地产市场?很难知道。房地产市场(的供应量)在一定程度上被之前人们锁定的低利率所冻结。人们不想卖掉他们的房子,因为他们的抵押贷款利率很低,而再融资的成本相当高。随着利率下降,人们将开始更多地搬家,这可能已经开始发生了。但请记住,当这种情况发生时,你有一个卖家,但在很多情况下,你也会有一个新买家。所以,你知道,有多少额外的需求会让我感到不明显。住房的真正问题是,我们已经拥有并将继续拥有不足的住房供应。所以这将是一个挑战。很难找到人们想住的地方的分区地块。住房的所有方面都越来越困难。你知道,我们要从哪里获得供应?这不是美联储能够真正解决的问题,但我认为随着利率正常化,你会看到房地产市场正常化。我的意思是,最终,通过降低通货膨胀率、使利率正常化、使住房周期正常化,这是我们能为家庭做的最好的事情。然后,供应问题必须由市场和政府来解决。

问题15:Just following up on some of the labor market talk earlier. You know, monetary policy operates with long and variable lags, and I‘m wondering how much you see being able to keep the unemployment rate from rate right raising too much comes from the fact that you’re starting to act now, and that‘s going to give people more room to run, versus just the labor market is strong. And then also, if I could following up on next question, do you see today’s 50 basis point move as partially a response to the fact that you didn‘t cut in July, and that sort of gets you to the same place.

货币政策的运作具有长期和可变的滞后性,我想知道你认为能够阻止失业率上升太多的程度有多大,这要归功于你现在开始采取行动,这将给人们更多的回旋余地,而不是仅仅因为劳动力市场强劲。然后,如果我可以跟进下一个问题,你是否认为今天降息50个基点是对你在7月没有降息这一事实的回应和补偿?

回答15:So you‘re right about lags, but I would just point to the overall economy. You have an economy that is growing at a at a solid pace. If you look at forecasters or talk to companies, they’ll say that they think 2025 should be a good year too. So there‘s no sense in the US economy. Basically fine, if you talk to market participants. I mean, I mean, you know, business people who are actually out there doing business. So I think, you know, I think we, I think our move is timely. I do. And as I said, you can, you can see our, our our 50 basis point move as as a commitment to make sure that we don’t fall behind. So you‘re really asking about your second question. You’re asking about July. And I guess if you, if you ask, you know, if we gotten the July report before the meeting, would we have cut we might well of we didn‘t make that decision, but you know that we might well have, I think that’s not, you know, that doesn‘t really answer the question that we ask ourselves, which is, let’s look, you know, when at this meeting, we‘re looking back to the July employment report, the August employment report, the two CPI reports, one of which came, of course, during blackout, and all the other things that I mentioned, we’re looking at all of those things and we‘re asking ourselves, what’s the right what‘s our what’s the policy stance we need to move to? We knew it‘s clear that we clearly, literally everyone on the committee agreed that it’s time to move. It‘s just how big, how fast you go, and what do you think about the pass forward? So this decision we made today had broad support on the committee, and I’ve discussed the path ahead. Elizabeth,

你对滞后的看法是对的,但我只想指出整体经济。美国经济正在稳步增长。如果你看看预测者或与公司交谈,他们会说他们认为2025年也应该是好年头。所以美国经济基本上没问题。我认为我们的举措是及时的。你可以把我们的50个基点调整看作是一种承诺,以确保我们不会落后。如果在7月份FOMC会议前拿到当月非农数据,我们当时是否会降息呢,可能会,但是我认为这并没有真正回答我们问自己的问题,那就是,让我们看看,在这次会议上,我们回顾了7月份的就业报告、8 月份的就业报告、两份CPI报告,其中一份是在静默期内发布的,以及我提到的所有其他事情,我们正在研究所有这些事情,我们在问自己,什么是正确的,我们需要采取什么样的政策立场?我们知道,很明显,委员会中的每个人都同意是时候采取行动了。只是规模有多大,速度有多快,你对未来利率路径有什么看法?所以我们今天做出的这个决定得到了委员会的广泛支持,我已经讨论了未来的道路。

问题16:mortgage rates have already been dropping in anticipation of this announcement. How much more should borrowers expect those rates to drop over the next year?

按揭抵押贷款利率已经在预期降息时就下降了。预计明年这些利率还会下降多少?

回答16:Very hard for me to say that‘s from our standpoint. I can, I can’t really speak the mortgage rates. I will say, you know, that will depend on on how the economy evolves. Our our intention, though, is we think that our policy was appropriately restrictive. We think that it‘s time to begin the process of recalibrating it to a level that’s more neutral, rather than restricted. We expect that process to take some time, as you can see in the projections that we released today, and as if things work out according to that forecast, other rates in the economy will come down as well. However, the rate at which those things happen will really depend on how the economy performs. We can‘t see, we can’t look a year ahead and know what the economy is to be doing.

从我们的角度来看,我很难说。我不能真正谈论抵押贷款利率。我会说,这取决于经济如何发展。但我们的意图是,我们认为我们的政策是适当的有限制性。我们认为是时候开始将其重新调整到更中性而不是维持限制性的水平了。我们预计这个过程需要一些时间,正如你在我们今天发布的预测中所看到的,如果事情按照预测发展,经济中的其他利率也会下降。然而,这些事情发生的速度实际上取决于经济的表现。我们无法看到,我们无法展望一年后的经济情况。

What‘s your message to households who are frustrated that home prices have still stayed so high as rates have been high? What do you say to those households?

追问:对于那些因为利率居高不下而房价居高不下的家庭,您有什么话要说?

Well, I can what I can say to the public is that we had the highest we had a burst of inflation.Many other countries around the world had had a similar burst of inflation. And when that happens, part of the answer is that we raise interest rates in order to cool the economy off in order to reduce inflationary pressures. It‘s not something that people experience as pleasant, but at the end, what you get is low inflation restored. Price stability, restored. And a good definition of price stability is that people in their daily decisions, they’re not thinking about inflation anymore. That‘s where everyone wants to be, is back to what’s inflation, you know, just keep it low, keep it stable. We‘re restoring that. So what we’re going through now, really, it restores it will benefit people over a long period of time. Price stability benefits everybody over a long period of time, just by virtue of the fact that they don‘t have to deal with inflation. So that’s what‘s been going on. And I think we’ve made real progress. I completely we don‘t tell people how to think about the economy, of course, and of course, people are experiencing high prices, as opposed to high inflation, and we understand that’s painful.

我可以告诉公众的是,我们经历了最高的通货膨胀,世界上许多其他国家也经历过类似的通货膨胀。当这种情况发生时,部分解决办法是我们提高利率,以便冷却经济,从而减少通胀压力。这不是人们会感到愉快的事情,但最终,我们得到的是恢复低通胀。恢复价格稳定。价格稳定的一个好定义是,人们在日常决策中不再考虑通货膨胀。这就是每个人都希望的,即保持通胀在低位和稳定。我们正在恢复这种状态。所以我们现在正在经历的,真的,恢复这种状态将在很长一段时间内使人们受益。价格稳定在很长一段时间内使每个人都受益,因为他们不必应对通货膨胀。这就是正在发生的事情。我认为我们已经取得了真正的进步。我完全不会告诉人们应该如何看待经济,当然,人们正在经历高物价,而不是高通胀,我们理解这是痛苦的。

问题17:I was wondering if you could go through you said just at the beginning that coming into the blackout, there was like an open thought of 25 or 50. You know, the fact that we‘re either 25 or 50, I would sort of argue that when we had those two last speeches by Governor Waller and New York President John Williams, that they were, they were sort of saying that maybe a gradual approach was going to win the day. I mean, I sort of want to ask a seven part question about this. But I mean, could you talk, would you have cut rates by 50 basis points if the market had been pricing in, like, low odds of a 50 point move, like they were last Wednesday. You know, after the CPI number came out, there’s a really small probability of a 50 point cut. Does it play playing your consideration at all.

美联储官员刚进入公开讲话的静默期时,人们对于降息25个基点还是50个基点持开放态度。理事沃勒和纽约联储主席威廉姆斯的讲话也说渐进式降息会占上风。如果市场定价的是不太可能降息50个基点,您这次还会大幅降息吗?市场的定价押注是否影响到美联储的决策?

回答17:Thank you. We‘re always going to try to do what we think is the right thing for the economy at that time. That’s what we‘ll do, and that’s what we did today.

我们总是会尽力做我们认为对当时的经济有利的事情。这就是我们要做的,也是我们今天所做的。

问题18:you‘ve mentioned how closely you’re watching the labor market, but you also noted that payroll numbers have been a little bit less reliable lately because of the big downward revisions. Does that put your focus overwhelmingly on the unemployment rate? And given the SEP projection of 4.4 basically being the peak in the cycle, would going above that be the kind of thing that would trigger another 50 basis point cut.

您提到过您密切关注劳动力市场,但您也指出,由于遭遇大幅下修,最近就业人数的可靠性有所下降。这是否意味着您的注意力主要集中在失业率上?鉴于SEP预测的4.4%基本上是周期中的失业率峰值,超过这一水平是否会引发另一次50个基点的大幅降息?

回答18:So we will continue to look at that broad array of labor market data, including the payroll numbers. We‘re not discarding those. I mean, we’ll certainly look at those, but we will mentally tend to adjust them based on the Q, C, E, W adjustment, which you referred to. There isn‘t a bright line, you know, it will be the light that the unemployment rate’s very important, of course, but there isn‘t a single statistic or a single bright line over which that thing that might move, that would dictate one thing or another. We’ll look at each meeting, we‘ll look at all the data on inflation, economic activity and the labor market, and we’ll make decisions about is our policy stance where it needs to be to, you know, to foster over the medium term, our mandate goals. Yeah, so I can‘t, I can’t say we, we have a bright line in mind.

我们将继续关注广泛的劳动力市场数据,包括非农就业。我们不会放弃这些数据。我的意思是,我们肯定会关注这些数据,但我们在心理上会倾向于根据您提到的 QCEW 调整来调整它们。没有一条明确的界线,当然,失业率非常重要,但没有一个统计数据或一条明确的界线可以决定这件事或那件事。我们会在每次会议上,查看有关通货膨胀、经济活动和劳动力市场的所有数据,并决定我们的政策立场,以便在中期内促进我们的授权使命。所以我不能说我们心中有一条明确的界线。

问题19:I know that you discussed earlier how the Fed does whatever the right thing is and nothing else factors in. But in general, can you talk about whether or not you believe a sitting US president should have a say in fed decisions on interest rates? Because that‘s something that former President Trump, who obviously points of view, has previously, suggested, and I know the Fed is designed to be independent, but why can you tell the public why you view that so important?

我知道您之前讨论过美联储会做正确的事情,其他因素都不考虑。但总的来说,您能否谈谈您是否认为现任美国总统应该对美联储的利率决策有发言权?因为这是前总统特朗普之前提出的,他显然有自己的观点,我知道美联储的设计初衷是独立的,但您为什么能告诉公众您认为这一点如此重要呢?

回答19:Sure, countries that are sort of like the United States, all have what are called independent central banks. So that that‘s, that’s the idea, is that, you know, I think the data are clear that countries that have independent central banks, they get lower inflation. It’s just maximum employment and price stability on behalf of all Americans, and that‘s how the other central banks are set up to it. It’s a good institutional arrangement which has been good for the public, and I hope and strongly, strongly believe that it will. You know, continue.

当然,像美国这样的国家都有所谓的独立央行。这就是我们的想法,我认为数据清楚地表明,拥有独立央行的国家通胀率较低。我们只是为所有美国人实现最大化就业和价格稳定,其他央行就是这样建立的。这是一个对公众有利的良好制度安排,我希望并坚信它会继续下去。

问题20:a couple regulatory developments in the past week that I want to ask you about. First last week, Vice Chair for supervision, Michael Barr outlined his views for the changes to the Basel three end game. I‘m wondering if you are in line with him on those changes should be if those have support the board in a broad way that you’re looking for, and if you think the other agencies are also fully on board with that approach

我想问您关于过去一周的几个监管发展。首先,上周美联储负责监管的副主席Michael Barr概述了他对巴塞尔协议三监管规则变更的看法。我想知道您是否同意他的观点,是否其他机构也完全支持这种方法?

回答20:So the answer to your question is that, yes, those those changes were negotiated between the agencies with my support and with my involvement, with the idea that we were going to re propose, we propose the changes that we, that Vice Chair Barr talked about, and then take comment on them. So yes, that that is, you know, that‘s happening with my support. That’s not a final proposal, though. You understand, we‘re putting them out for comment. We’re going to take comment and make appropriate changes that we don‘t have a, we don’t have a calendar date for that. And as for the other agencies, you know, the idea is that we‘re all moving together. We’re not moving separately. So that I don‘t, I don’t know exactly where that is, but the idea is that we will move as a group to put this again out for comment, and then, you know, it‘ll, it’ll come the comments will come back 60 days later, and we‘ll dive into them, and we’ll try to bring this to a conclusion sometime in the first half of next year.

对你问题的回答是“是的”,这些变化是在我支持和参与下由各机构协商达成的,我们的想法是重新提出,我们提出巴尔副主席谈到的变化,然后征求意见。所以是的,那是在我的支持下发生的。但这不是最终提案。你知道,我们正在征求意见。我们将征求意见并做出适当的改变,但我们没有具体的日期。至于其他机构,你知道,我们的想法是我们都一起行动。我们不会分开行动。所以我不知道具体在哪里,但我们的想法是,我们将作为一个团队再次将这个问题提出来征求意见,然后,你知道,60 天后我们会收到评论,我们会深入研究它们,并尝试在明年上半年的某个时候得出结论。

Then yesterday, there were merger reform finalizations from the other bank regulators. What does that have to do to align itself on merger?

追问:昨天,其他银行监管机构也敲定了合并改革方案。这对合并有什么影响?

You know, I would, I would bounce that question to Vice Chair Barr. It‘s a good question, but I don’t have that today. Thanks Jennifer for the last question.

你知道,我会把这个问题转交给巴尔副主席。这是个好问题,但我今天没有答案。

问题21:you said earlier that the decision today reflects with appropriate recalibration, strength in the labor market that can be maintained in the context of moderate growth, even though the policy statement says you view the risks to inflation and job growth as roughly balanced, given what you‘ve said. Though today, I’m curious, are you more worried about the job market and growth than inflation? Are they not roughly balanced?

您之前说过,今天的决定反映了经过适当调整后,劳动力市场在温和增长的背景下仍能保持强劲,尽管政策声明中说,您认为通胀和就业增长的风险大致平衡,不过我很好奇,您是否更担心就业市场和增长而不是通胀?它们不是大致平衡的吗?

回答21:No, I think, I think, and we think they are now roughly balanced. So if you go back for a long time, the risks were on inflation. We had historically tight labor market, historically tight. There was a severe labor shortage, so very, very hot labor market, and we had inflation way above target. So you know that said to us, concentrate on inflation. Concentrate on inflation. And we did for a while, and we and we kept at that, that the stance that we put in place 14 months ago was a stance that was focused on bringing down inflation. Part of bringing down inflation, though, is is cooling off the economy, and a little bit cooling off the labor market. You now have a cooler labor market, in part because of of our activity. So what that tells you is it‘s time to change our stance. So we did that. The sense of the change in the stance is that we’re recalibrating our policy over time to a stance that will be more neutral. And today was we, I think we made a good, strong start on that. I think it was the right decision, and I think it should send a signal that we, you know, that we‘re committed to coming up with a good outcome here,

不,我认为,而且我们认为现在它们大致平衡了。所以如果你回顾很长一段时间,风险在于通货膨胀过高。我们的劳动力市场处于历史性紧张时期。劳动力严重短缺,因此劳动力市场非常非常火爆,而且通货膨胀率远高于目标。所以你知道,这告诉我们,要集中精力应对通货膨胀。我们确实这样做了一段时间,并且我们一直坚持这样做,14个月前我们制定的立场是专注于降低通货膨胀。然而,降低通货膨胀的一部分是冷却经济,以及稍微冷却劳动力市场。现在劳动力市场冷却了,部分原因是我们的活动。所以这告诉你是时候改变我们的立场了。所以我们这样做了。立场改变的意义在于,我们正在随着时间的推移重新调整我们的政策,使其立场更加中立。而今天,我认为我们在这方面取得了良好的开端。我认为这是正确的决定,我认为这应该发出一个信号,表明我们致力于达成一个好的结果。

to a shock now that could tip it into recession?

追问:大幅降息是否会令市场震惊并觉得经济衰退临近呢?

I don‘t think so. I don’t there‘s as I look, well, let me look at it this way. I don’t see anything in the economy right now that suggests that the likelihood of a recession, sorry, of a downturn is elevated. I Okay I don‘t see that, you see you see growth at a solid rate. You see inflation coming down and you see a labor market that’s still at very solid levels. It‘s so, so I don’t really see that now.

我不这么认为。目前,我没有看到任何迹象表明经济衰退的可能性增加。你看到经济增长率稳定。你看到通货膨胀率下降,你看到劳动力市场仍然处于非常稳定的水平。事实就是如此,所以我现在真的看不到这一点。■

降息50BP的情理之中与意料之外——美联储2024年9月议息会议解读

平安首经团队:

钟正生 投资咨询资格编号:S1060520090001

张 璐 投资咨询资格编号:S1060522100001

范城恺 投资咨询资格编号:S1060523010001

核心观点

美国时间2024年9月18日,美联储大幅降息50BP,并公布最新经济预测。市场感受“先鸽后鹰”:10年美债收益率和美元指数先跌后涨,美股三大指数先涨后跌,黄金现价创新高后回落。

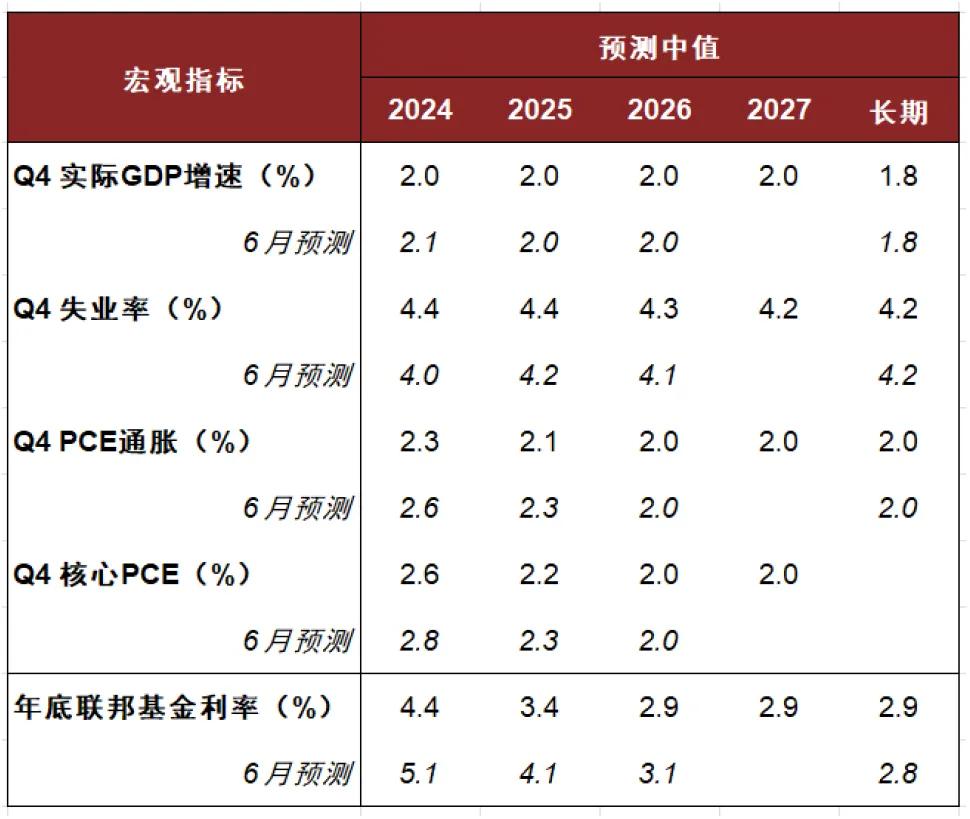

会议声明与经济预测:大幅降息50BP。美联储理事鲍曼在本次会议中投下反对票,其更赞成降息25BP。本次声明新增“委员会已经获得更大信心,通胀能够持续迈向2%目标”。经济预测基本维持2024-2025年增长预测,下修PCE和核心PCE预测,上修失业率预测。点阵图显示,在19位官员中,认为2024年内累计降息不超过75BP的有9位,其余10位认为累计降息不低于100BP,即大多数官员暗示年内的另外两次会议中仅降息1-2次、每次25BP。

鲍威尔讲话:“校准”,迈向“中性利率”。总的来看,鲍威尔讲话试图将本次大幅降息定义为一次“校准”,同时不断强调就业市场绝对水平仍然强劲,不希望市场解读为一次“紧急降息”,也不希望市场线性外推降息节奏。鲍威尔强调,本次降息并不意味着美联储“落后”,另一方面也说明美联储“不愿落后”。就业方面,鲍威尔强调当前就业已弱于2019年水平,但仍接近“最大就业”状态,没有看到衰退迹象;通胀方面,鲍威尔强调美联储还没有宣布抗击通胀的胜利,但是对通胀回落至目标水平很有信心。

政策逻辑:降息50BP的情理之中与意料之外。降息50BP的“情理之中”在于,美国就业市场走弱的斜率较为陡峭,通胀也较快回落,就业和通胀形势快速回到“平衡”状态,美联储维持“限制性利率”显得不合时宜,需要尽快迈向“中性利率”。但是,经济和通胀上行风险也是降息后可能出现的“意料之外”。一方面,当前美国经济增长趋势较强,与就业市场的走弱相悖。另一方面,从动态角度看,美联储降息可能进一步增大美国经济和通胀上行风险。我们倾向认为,美联储年内合理的降息幅度为100BP,即后续两次会议各降25BP,以防止金融条件不必要地过快放松。

市场展望:区分降息前后的行情。历史经验显示,美联储首次降息前,美债、黄金等通常受益;首次降息后,多数资产价格波动风险反而阶段增大。本轮美联储开启降息相对较晚,这也令首次降息50BP的幅度看起来较为激进。但这也说明,本轮美联储政策的灵活性较强。我们认为,首次降息50BP对经济和市场整体影响更偏积极。此外,本轮资产走势需要结合降息影响,以及美国大选、日本加息等宏观背景综合判断。

风险提示:美国就业超预期走弱,美国经济和通胀超预期上行,美国金融风险超预期上升等。

2024年9月美联储议息会议不寻常地以50BP开启降息周期,但并未完全脱离市场预期。降息50BP的“情理之中”在于,美国就业市场走弱的斜率较为陡峭,通胀也较快回落,就业和通胀形势快速回到“平衡”状态,美联储维持“限制性利率”显得不合时宜,需要尽快迈向“中性利率”。但是,经济和通胀上行风险也是降息后可能出现的“意料之外”。我们倾向认为,美联储年内合理的降息幅度为100BP,即后续两次会议各降25BP,以防止金融条件不必要地过快放松。本轮美联储政策的灵活性较强,传递了政策“不愿落后”的决心,首次降息50BP对经济和市场整体影响可能更偏积极。

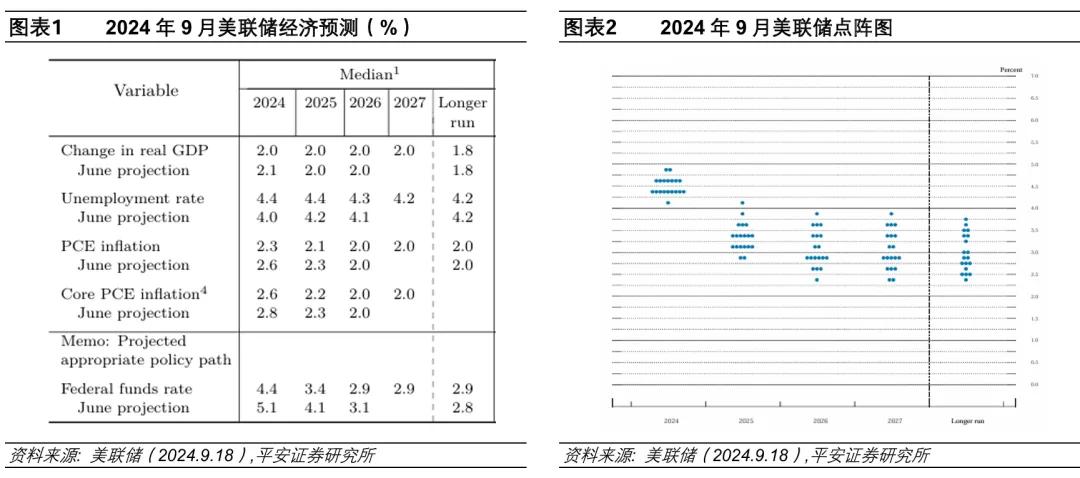

1. 会议声明与经济预测:大幅降息50BP

美联储2024年9月议息会议声明,将联邦基金目标利率下调50BP至4.75-5.00%区间。同时,美联储相应下调其他政策利率:1)将存款准备金利率下调至4.9%;2)将隔夜回购利率下调至5.0%;3)将隔夜逆回购利率下调至4.8%;4)将一级信贷利率维持下调至5.0%。缩表方面,美联储维持每月被动缩减250亿美元国债和350亿美元MBS的节奏不变。值得一提的是,美联储理事鲍曼在本次会议中投下反对票,其更赞成降息25BP,一定程度上体现了政策的分歧。

经济和政策描述部分,9月会议声明主要的改动包括:1)在就业描述上,将“新增就业有所放缓(moderated)”改为“新增就业放缓(slowed)”;2)通胀描述上,将“通胀有所缓解,但仍然较高”改为“通胀进一步向委员会的2%目标迈进,但仍然较高”;3)风险评估上,新增“委员会已经获得更大信心,通胀能够持续迈向2%目标”;并将就业和通胀风险的描述由“迈向更好的平衡”改为“已经基本处于平衡”。

美联储2024年9月发布的经济预测(SEP),相较2024年6月的主要变化包括:

1) 经济增长:将2024年经济增长预测由2.1%小幅下修至2.0%,维持2025和2026年经济增长预测为2%,维持长期经济增长率为1.8%。

2) 就业:将2024年底失业率预测由4.0%明显上修至4.4%,将2025和2026年失业率预测同时上修0.2个百分点分别至4.4%和4.3%,维持长期失业率预测为4.2%。

3) 通胀:将2024年PCE和核心PCE通胀率分别下修0.3个0.2个百分点至2.3%和2.6%,将2025年的这两个指标小幅下修至2.1%和2.2%,维持2026年以后及长期通胀预测为2.0%。

4) 利率:将2024年末政策利率中值预测由5.1%大幅下修至4.4%,将2025年政策利率预测由4.1%下修至3.4%,将长期政策利率小幅上修0.1个百分点至2.9%。

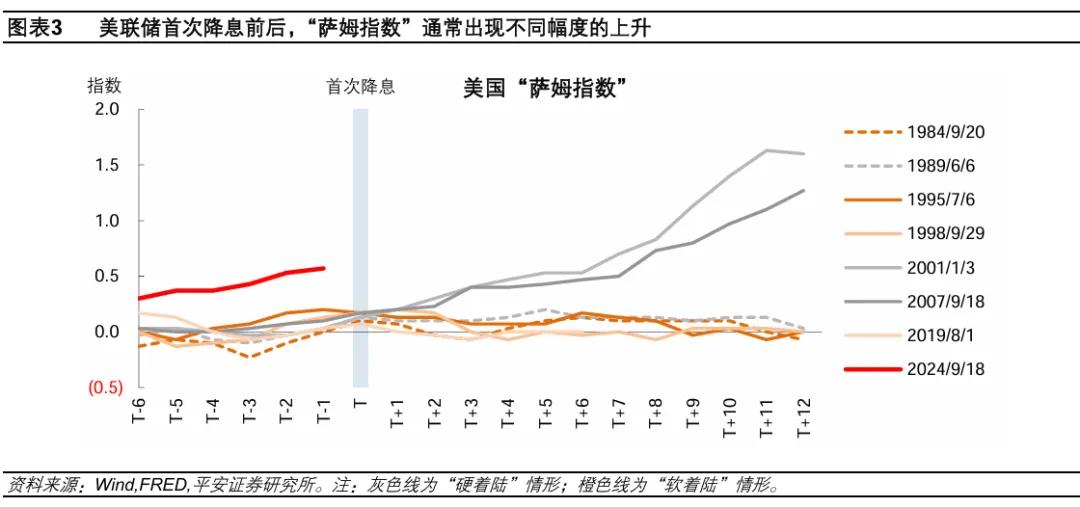

5) 点阵图:在19位官员中,认为2024年内累计降息不超过75BP的有9位,其余10位认为累计降息不低于100BP,即大多数官员暗示年内的另外两次会议中仅降息1-2次、每次25BP。其中,有2位预计年内不再降息,有1位预计年内还会有1次50BP的降息。有12位认为2025年末的政策利率在3-3.5%区间。

9月会议声明和经济数据公布后,市场短暂交易宽松:10年美债收益率下行4BP至3.65%,美股三大指数短线拉升,美元指数由100.8附近下行至100.3的低点,黄金现价短线升破2600美元/盎司大关。

2. 鲍威尔讲话:“校准”,迈向“中性利率”

总的来看,鲍威尔讲话试图将本次大幅降息定义为一次“校准”,同时不断强调就业市场绝对水平仍然强劲,不希望市场解读为一次“紧急降息”,也不希望市场线性外推降息节奏。鲍威尔强调,本次降息并不意味着美联储“落后”,另一方面也说明美联储“不愿落后”。就业方面,鲍威尔强调当前就业已弱于2019年水平,但仍接近“最大就业”状态,没有看到衰退迹象;通胀方面,鲍威尔强调美联储还没有宣布抗击通胀的胜利,但是对通胀回落至目标水平很有信心。

鲍威尔讲话后,市场修正“宽松交易”:10年美债收益率反弹至3.71%,超过降息前水平,日内累涨6BP;美股三大指数由涨转跌,分别收跌0.25-0.31%;美元指数最高升至101附近;黄金现价回落至2560美元/盎司附近。

具体来看:

1)关于降息50BP。多位记者就本次的“不寻常降息”提问,旨在探讨降息50BP的原因、以及释放的信号。鲍威尔回复中,多次使用“校准(recalibrate)”一词,认为降息50BP是在适当调整利率水平,向“中性利率”水平靠近;未来美联储降息加速、减速或暂停都有可能。“新美联储通讯社”华尔街日报记者Nick提问:降息50BP是一种“追赶”,还是一种未来降息节奏的“示范”?鲍威尔称,其不认为美联储“落后”,但另一方面本次降息也说明美联储“不愿落后”。其称,相比很多国家,美联储在降息方面已经很有耐心;不认为这是新的降息节奏(new pace),而只是一次校准。有记者让鲍威尔总结一下本次降息想要释放的信号。鲍威尔总结道,其想(通过本次降息)维持当前较好的经济状况。

2)关于就业市场。本次会议中,大约有三分之一的记者的问题都围绕就业市场,因近期就业数据的走弱是触发美联储本次大幅降息的主要原因。总结而言,鲍威尔试图传递以下几个信息:当前的就业市场可以被认为略弱于2019年水平,但是就业市场的绝对水平仍然是强劲的,十分接近“最大就业”状态;美联储希望维持当前的就业市场状态;美联储下次会议前还有2份就业数据需要观察;可能的风险在于未来职位空缺率进一步下降可能更直接地反映在失业上。但是,记者们频繁问道,美联储为何有信心就业市场能够维持目前的水平(而不是进一步走弱)?鲍威尔似乎没有给出令人满意的解释。不过,当被问及衰退风险时,鲍威尔也较有信心地回答称,没有看到任何衰退的迹象。

3)关于通胀。本次会议围绕通胀的讨论不多。有记者问,美联储是否可以宣布抗击通胀已取得胜利。鲍威尔明确回答:No!其称,希望看到通胀水平在2%附近维持一段时间,但近期通胀的进展也令美联储受到鼓舞。有记者问如何看待住房通胀的粘性?鲍威尔称,住房通胀只是通胀的一个方面,其回落的方向是明确的,只是需要更长时间;但其认为只要住房市场仍在掌控之中,其相信核心PCE及住房通胀会回到目标水平。

4)关于长期利率。有记者关注点阵图中暗示的2025年利率,认为其仍处于“限制性利率”。鲍威尔称,关于“中性利率”有不同的测算,但核心思想是,我们只能根据结果来倒推中性利率(原话是:“We know it by it works”)。有记者问长期利率是否会高于疫情前水平?鲍威尔称,个人感觉利率水平不会回到从前。

5)关于大选。仍有两位记者询问大选会否影响美联储决策。鲍威尔的回答似乎比上次会议更有耐心,其强调已经经历了第四次大选,且美联储的决策都是集体决策,不服务于任何党派而是全体美国人,只会做认为正确的事情。当被问及为何独立性如此重要时,鲍威尔称全球范围看,拥有货币政策独立性的国家通胀水平会更低。

3. 政策逻辑:降息50BP的情理之中与意料之外

美联储不寻常地以50BP开启降息周期,但也并未完全脱离市场预期。我们在报告《美联储“首降”前的争议》中提到,9月12日以来,华尔街日报及美联储前高官杜德利等“吹风”,探讨首次降息25BP还是50BP更合适,此后市场加大了对首次降息50BP的押注。截至9月18日降息前,CME利率期货认为本次会议降息50BP的概率为59%。

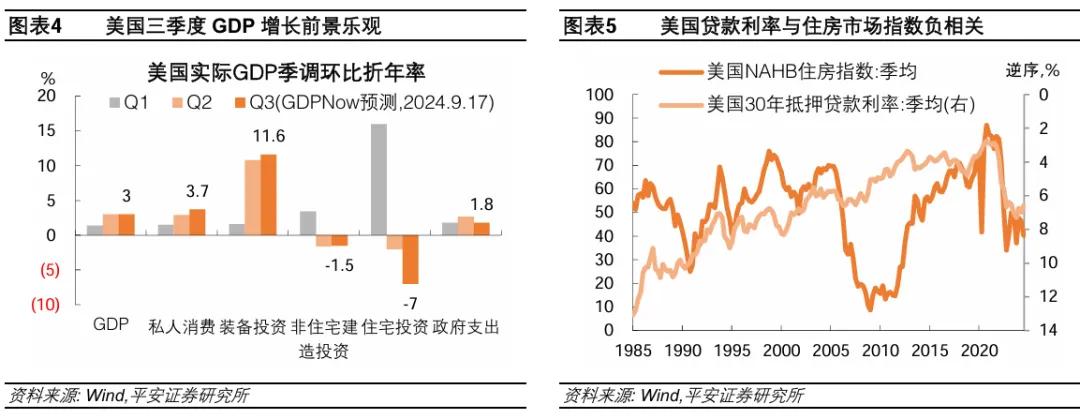

如何理解美联储首次降息50BP?我们认为主要有两方面“情理之中”:一方面,近2-3个月美国就业市场走弱的斜率较为陡峭,增强了降息的紧迫性。我们对比1982-2019年的其他7轮降息周期,本次降息前失业率上升的斜率最为陡峭。这反映在“萨姆指数”首次在降息前就上升超过0.5,此前历次降息前萨姆指数均不超过0.2。另一方面,随着美国通胀也较快回落,就业和通胀形势快速回到“平衡”状态,美联储维持“限制性利率”显得不合时宜,需要尽快迈向“中性利率”。

不过我们也想指出,美联储大幅降息后,未来可能出现“意料之外”,即美国经济和通胀上行风险尚不能完全排除。

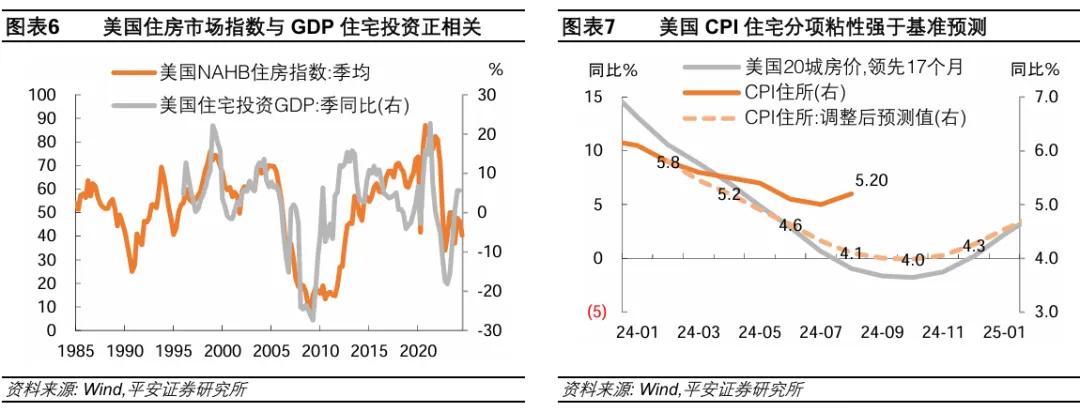

一方面,当前美国经济增长趋势较强,与就业市场的走弱相悖。据亚特兰大联储GDPNow模型,截至9月17日(美国零售数据等公布后),模型预测美国三季度实际GDP环比折年率高达3.0%,今年一、二季度这一增速已分别达到1.4%、3.0%。我们测算,假设三季度继续增长3.0%,即使四季度环比增长为0,美国2024年全年经济增速仍将高达3.8%,远超过美联储本次最新预测的2.0%。

另一方面,从动态角度看,美联储降息可能进一步增大经济和通胀上行风险。以对利率最为敏感的房地产市场为例,我们初步估算,当本轮30年抵押贷款利率上升1个百分点,美国NAHB住房指数平均下降13.5个单位;假设年内美联储降息100BP,30年抵押贷款利率也下降100BP(实际幅度还取决于市场利率预期),基于住房指数和GDP住宅投资的OLS相关性模型,这可能拉动四季度GDP住宅投资同比增速4.3个百分点,并拉动四季度GDP同比增速0.15个百分点。通胀方面,当前美国CPI住所分项的粘性,已经明显强于我们基于房价和房租相关性的基准预测。未来,如果美国房地产市场得益于降息而较快复苏,房价及房租通胀的粘性可能进一步增强。

如何看待美联储合理的降息节奏?我们倾向认为,美联储年内合理的降息幅度为100BP,即后续两次会议各降25BP,以防止金融条件不必要地过快放松。

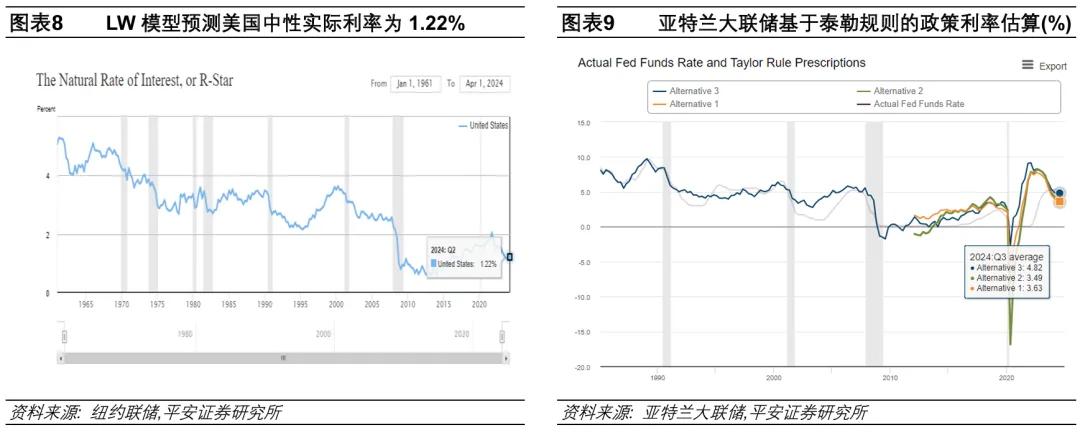

首先,美国中性名义利率大约为2.9-3.2%。根据纽约联储LW模型(Laubach-Williams model)最新测算,截至今年二季度,美国的“中性实际利率”水平为1.22%,如果加上2%的目标通胀水平,“中性名义利率”大致为3.2%;而美联储最新长期名义政策利率预测为2.9%。

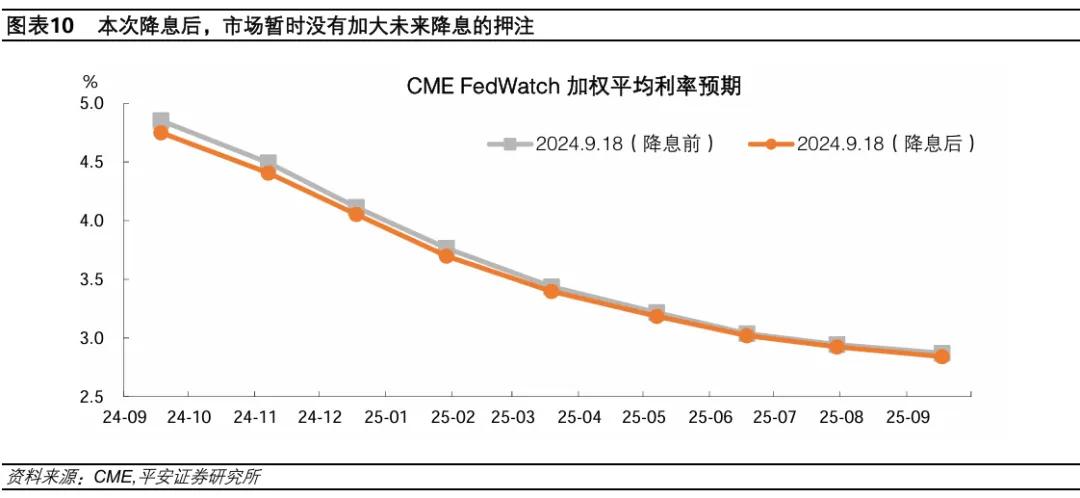

其次,当前经济状况需要政策利率略高于中性利率。根据泰勒规则,考虑到目前美国核心PCE略高于2%目标,失业率基本持平于长期失业率4.2%(美联储预测),而GDP增速似乎略高于2%的潜在增速水平(CBO预测),那么当前美联储合意的政策利率水平应该略高于3%,可能在3.5-4%左右(参考亚特兰大联储三种基准模型的预测结果为3.6-4.8%)。

最后,美联储可能还需控制降息速度,避免降息过快。如果仅基于当前美国经济增长、就业和通胀水平,美联储短期应有150BP左右的降息空间,从限制性利率回到“轻微”限制性利率。但是,考虑到较快降息可能增加经济和通胀反弹风险,美联储降息的节奏和幅度应更受限制。

4. 市场展望:区分降息前后的行情

我们在报告《美联储历次开启降息:经济与资产》中,探讨了美联储历次开启降息的历史经验对当下的启示。我们认为,如果未来不出现严重经济或金融市场冲击,“软着陆”仍是基准情形。本轮美联储开启降息相对较晚,这也令首次降息50BP的幅度看起来较为激进。但是这也说明,本轮美联储政策的灵活性较强,如鲍威尔所说的,本次降息也传递了政策“不愿落后”的决心。我们认为,首次降息50BP对经济和市场整体影响更偏积极。

历史经验显示,美联储首次降息前,美债、黄金等通常受益;首次降息后,多数资产价格波动风险反而阶段增大。此外,本轮资产走势需要结合降息影响,以及美国大选、日本加息等宏观背景综合判断。

具体来看:

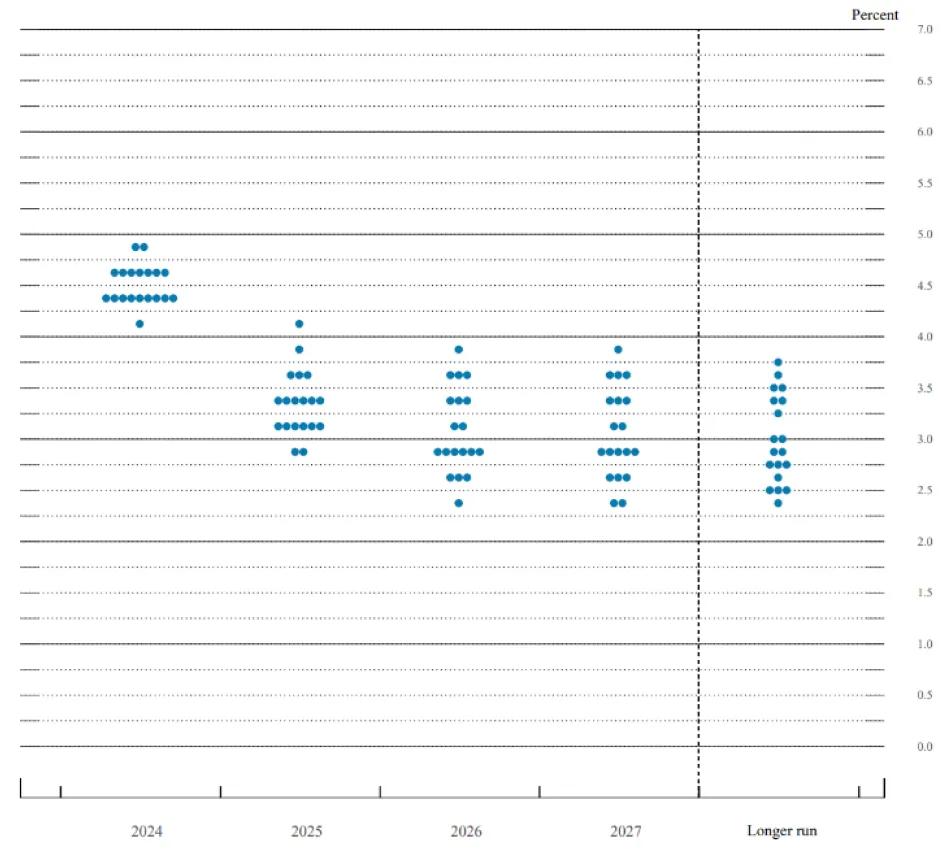

1)10年美债利率有可能在首次降息后1-2个月内阶段反弹,之后继续下行。本次降息后,市场暂时没有加大对美联储未来降息的押注。美联储较大幅度降息后,未来1-2个月的经济和就业市场更有望保持韧性,可能令美债利率阶段触底回升。

2)美元指数未必因降息下跌,但可能受日元升值拖累。短期需关注日本央行本周的会议,尽管目前市场预计本次加息的概率不高,但不排除年底继续加息,这可能令日元保持升值方向。

3)美股在首次降息后1-2个月的波动风险仍值得警惕,尽管大方向仍然积极。除降息影响外,美国大选也为市场增添了不确定性。

4)黄金在降息前已上涨较多,降息后较有可能盘整。历史经验显示,降息后的黄金胜率相对有限。

5)原油价格较可能在降息后保持震荡。美国经济走弱的担忧降温,或者产油国进一步减产,都有可能阶段阻止近期油价的跌势。

风险提示:美国就业超预期走弱,美国经济和通胀超预期上行,美国金融风险超预期上升等。■

中金:美联储为软着陆而大幅度降息

肖捷文 张文朗

本次会议的背景是近两个月来美国通胀放缓,同时就业市场出现走弱迹象。市场想知道美联储将如何回应这些边际变化,它的反应函数(reaction function)是什么?在会议之前,市场已经充分预期了这次的降息,不确定性在于降息幅度是25还是50个基点。

从利率决议来看,美联储采取了更大幅度的50个基点的降息,比我们预期的更激进。货币政策声明中指出,最近的通胀数据让决策者对于实现2%的通胀目标有了更多信心。与此同时,随着失业率上升,美联储也强调致力于最大化就业的目标(The Committee is strongly committed to supporting maximum employment…)。

美联储的行动表明,它的反应函数已经从关注通胀完全转向了关注就业。美联储主席鲍威尔在8月杰克逊霍尔会议上曾表示,“不欢迎就业数据进一步降温”。在这之后公布的8月份非农数据喜忧参半,失业率虽较7月份下降,但新增非农就业人数继续放缓。很显然,鲍威尔认为这一变化触发了他所讲的情况,因此在这次会议上希望兑现承诺,推动降息50个基点。

尽管鲍威尔在记者会上否认抗通胀取得胜利,但他现在似乎只关注就业。鲍威尔表示,希望失业率保持在当前水平,不再继续抬升。美联储官员们也预测,失业率将在今年底前进一步上升0.2个百分点,至4.4%。在2025和2026年,失业率都将稳定在4.4%附近。

我们认为这是一个信号,即美联储对失业率上升的容忍度很低,官员们不想冒险而破坏“软着陆”的美好前景。基于鲍威尔的表述,我们认为未来任何超过4.4%的失业率都可能触发更多降息。这也表明,在就业市场的数据没有稳定之前,美联储都将保持“鸽派”姿态。根据最新点阵图,在19名官员中,有10人预测今年底前至少还有两次降息,另外7人预测只有1次降息,2人预测不再降息。这表明多数官员倾向于年底前还需要继续降息,以确保失业率被控制在4.4%以下的充分就业范围内。

不过,这次降息50个基点也并非所有人的共识。在12名投票的官员中,11人投了赞成票,理事鲍曼投了反对票,她更倾向于降息25个基点。这也是自2005年以来首次有美联储理事投了反对票。另外比较微妙的是,在8月份非农数据公布后,美联储官员并未明确释放降息50个基点的信号,直到上周“静默期”开始后,才有消息称美联储正在考虑更大幅度的降息。这表明,决策者在降息25还是50个基点的问题上也有过犹豫。

往前看,由于美联储采取了更大幅度的降息,短期内经济软着陆的可能性将进一步上升。我们在此前报告《通向软着陆的经济与政策》中指出,历史上的软着陆通常都伴随降息,因为在大幅紧缩之后适度调整货币政策有助于避免过度紧缩。这一次,由于供给因素改善、通胀上行风险短期可控,美联储降息将支撑需求扩张,美国经济增长可能继续保持较高增速,从而提升软着陆的几率。美联储官员在最新预测中下调了对通胀的预测,对经济增长的预测保持不变,也表明了其对于软着陆的信心。

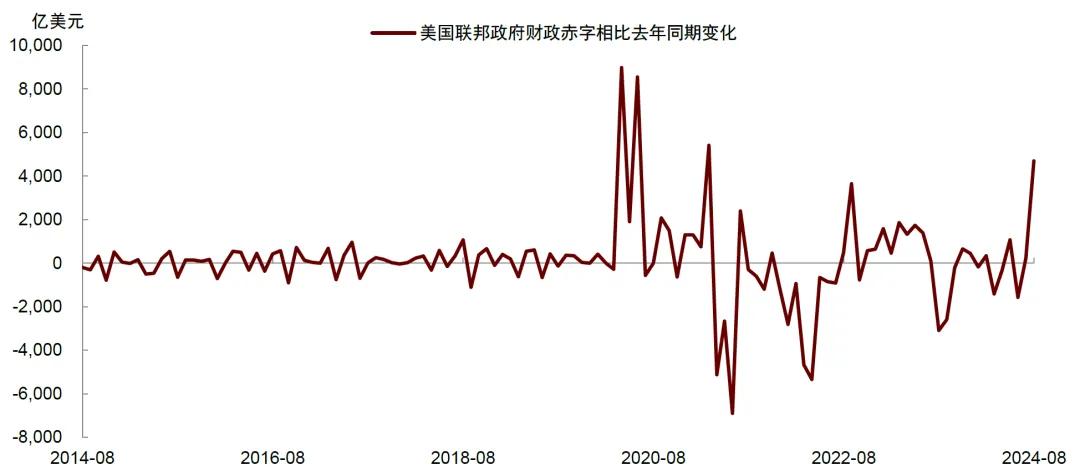

但中期来看,美国“宽财政,松货币”的政策组合可能增加通胀风险。美国财政部最新的数据显示,8月份财政赤字增加至3801亿美元,相比上月的赤字增加了1363亿美元,比去年同期的赤字增加了4693亿美元。从同比变动来看,8月份财政赤字增加幅度是过去三年的最高水平。此外,2024年1-8月累计财政赤字已经达到1.39万亿美元,相比去年同期增加了2800万亿美元,增幅高达25%。这些数据表明今年的财政政策不但没有收紧,反而还在继续扩张。扩张的财政本来就具有提振经济的效果,再加上美联储现在为了压低失业率而采取更大幅度的降息,这可能会导致经济在中期维度重新回到“不着陆”状态。届时如果供给因素不再改善,那么需求的反弹也或将推高通胀。今天美联储议息会议后美债收益率不跌反涨,收益曲线陡峭化,可能也反映了市场对于美联储激进降息可能带来长期通胀风险的关切。■

图表1:美联储9月利率点阵图

图表2:美联储对经济指标的预测(2024年9月)

图表3:美国财政赤字加速发力

中金:美联储“非常规”降息开局

刘刚 王子琳等

在市场热烈的期待和对经济“衰退”的担心中,美联储如期开启降息,这是2020年疫情以来的首次降息,也意味着2022年3月开启本轮加息周期、2023年7月停止加息后,本轮紧缩周期的结束。但降息幅度部分让市场“意外”,50bp的开局在历史上并不常见,上世纪90年代以来仅有2001年1月、2007年9月和2020年3月这三次。

图表:经济不是衰退,降息也不是衰退式降息

各类资产的反应更是纠结,美债、黄金、美元和美股都是先涨后跌,决议公布后因降息50bp开局而大涨,但收盘却因后续路径和经济前景而回调。会议前,尽管公布的通胀、就业等多项数据对于衰退和降息的“增量信息”有限,甚至零售、工业产出等还超预期,但市场押注美联储首次降息50bp的概率显著上升,对美联储政策操作“落后于曲线”的担忧加剧。与此同时,美股重回新高,美债和黄金上涨,美元弱,似乎在交易“宽松给够但增长不差”的组合。

图表:近期宽松交易推动金融条件转松

美联储开启降息后,尤其是本轮“非常规”降息和预期已经充分酝酿下,资产应该如何交易,是投资者普遍关心的问题。基于此前数篇专题报告的分析,并结合此次会议信息,我们分析如下。

会议的信息:首次降息50bp,年内再降息两次,整体幅度250bp;强调无衰退迹象,强调中性利率更高

此次会议在“非常规”降息50bp的同时,也调整了未来降息预期的“点阵图”和经济数据预测,同时鲍威尔在会后的新闻发布会上针对后续降息路径、经济前景重点传递了以下几点信息。

1)降息50bp是非常规开局,部分超出市场预期。此次降息50bp符合CME利率期货的预期,但却超出很多华尔街投行预测,同时也是“非常规”开局。历史上,降息50bp起步的情形只有在经济或市场紧急时刻才出现,例如2001年1月科技泡沫、2007年9月金融危机,2020年3月疫情等。

图表:1990年以来历轮降息周期幅度与背景

2)年内再降息两次共50bp,整体降息幅度250bp,低于会前CME期货的预期。更新的“点阵图”预计,年内将再降息两次共计50bp,2025年降息4次100bp,2026年2次50bp,加上此次50bp降息,使得整体降息幅度达到250bp,利率终点为2.75-3%。这一路径明显低于CME利率期货交易的2025年9月就要到达2.75-3%这一水平的斜率,一定程度上可能解释了收盘后美债利率的冲高。不过值得说明的是,由于降息预期的摇摆和“点阵图”的产生机制,距离当前越远的预期“可信度”越差,更多是作为对当前市场预期的比照。

3)鲍威尔不断强调此轮降息50bp不能作为新基准而线性外推,认为中性利率显著高于疫情前水平。考虑到降息50bp很容易引发美联储行动过慢的担心,鲍威尔在会后的新闻发布会上不断强调,此次降息并非美联储急于行动,是对当前就业市场环境的正常应对。同时,为了努力打消市场对于当前降息路径的线性外推,鲍威尔还强调,没有设定固定利率路径,可以加快,也可以放缓,甚至选择暂停降息,会根据每次会议情况而定。

此外,鲍威尔还提到认为中性利率显著高于疫情前水平,意味着最终利率终点也将维持在更高位置。此次经济数据调整中,美联储将中性利率从上次的0.8%,调高至0.9%

4)鲍威尔强调没有看到任何衰退迹象,劳动力市场降温,但通胀问题上并未取得胜利。由于降息50bp也更容易让市场有更大的经济“衰退”担忧,因此鲍威尔还强调并没有看到经济中有任何迹象表明衰退的可能性正在上升,试图用这种方式来对冲市场的担心。此次经济数据预测中比较大的变化是上调今年的失业率预测(从4%到4.4%,但稳定在这一位置),并下调PCE预测至2.3%。

图表:我们初步测算,整体CPI和核心CPI同比都将延续回落态势

图表:劳动力市场走弱风险或在上升

整体来看,我们认为此次会议美联储的确看到了就业市场的疲弱,否则也不会采取开局就降息50bp的“非常规”操作,一定程度上也回应了市场的“呼声”。同时,也在努力营造一种“领先于市场”,随时可以做得更多,但又不想让市场担心因为大幅衰退压力而被迫着急做得更多的形象。从市场的反应来看,不着急做的更多的确起到了效果,解释了避险资产的下跌,但经济“衰退”压力还未能完全让市场信服,解释了风险资产同样的回调。

降息的路径:非衰退压力下,更快降息反而会使后续路径放缓,宽松效果其实已经开始显现

尽管开局降息50bp,但结合乐观指引与当前数据,我们依然认为“软着陆”是基准情形。一个有意思的悖论是,更为陡峭的初始斜率反而使得后续降息路径放缓,是因为宽松会更快地在利率敏感部分发挥效果,如地产。当然,这意味着后续几个月公布的经济数据就至关重要,能够“立得住”,只要不大幅恶化,甚至还出现改善,都可以进一步佐证美联储想要传递的“更快降息但增长不差”信息,届时风险资产将表现更好,而避险资产则接近尾声。

实际上,虽然还没有降息,但宽松效果其实已经开始显现,体现在:1)房地产出现量价齐升迹象:30年按揭利率跟随10年美债快速降至6.4%后,已经低于7%的平均租金回报率,这使得7月美国成屋和新屋销售时隔5个月后再度回暖,美国成屋销售5个月来首次正增长,具有领先性的新屋销售7月也环比增长10%。此外,再融资需求随着按揭利率下行也已经回暖,7月CPI中等量租金(OER,与房地产预期高度相关)时隔5个月再度回升。

图表:30年按揭利率跟随10年美债降至6.2%后,美国成屋销售转为正增长

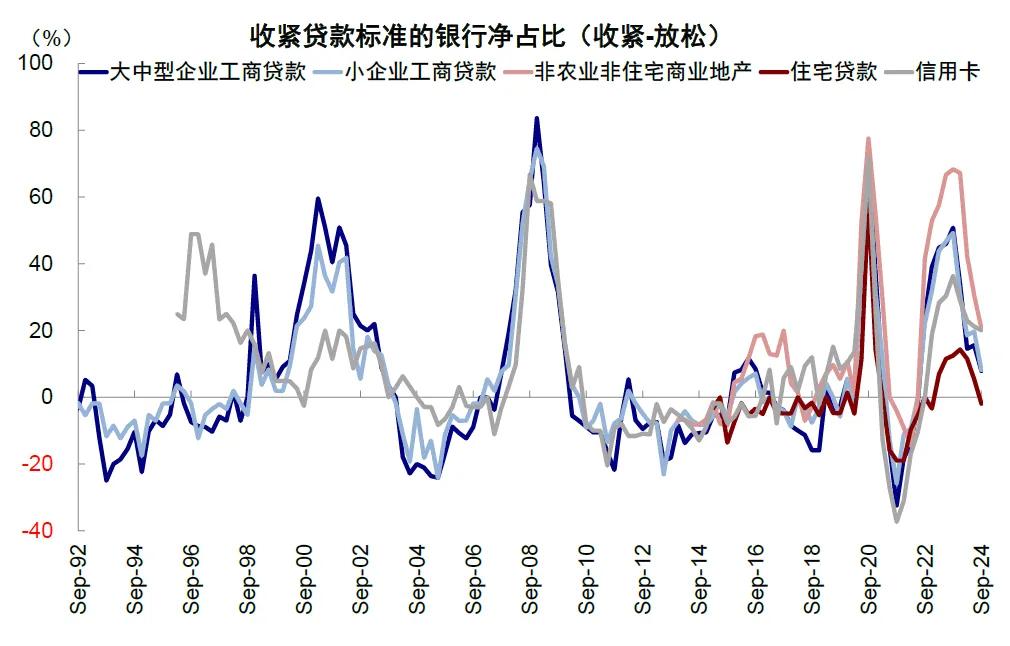

2)间接融资:三季度收紧贷款标准的银行占比已经大幅回落,其中住宅贷款标准甚至转为放松(收紧-放松的银行占比为-1.9%)。

图表:三季度收紧贷款标准的银行占比已经大幅回落

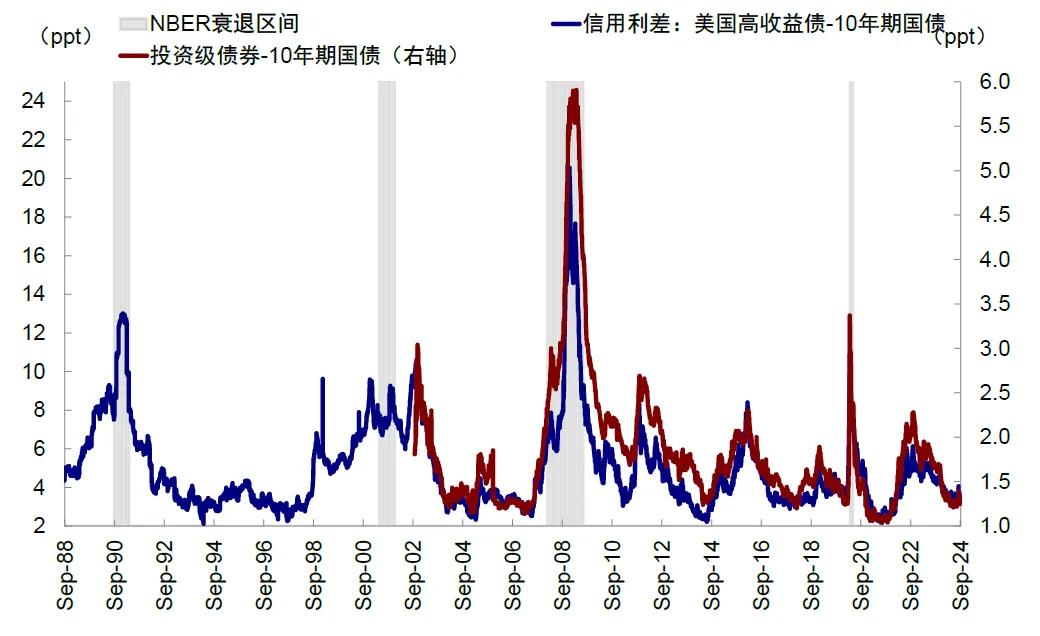

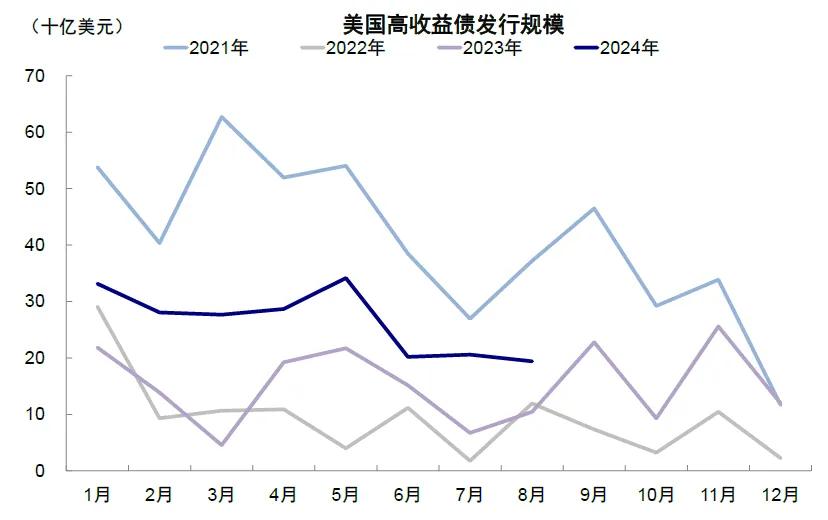

3)直接融资:投资和高收益债信用利差分别处于14.6%和32.7%的历史低位,加上基准利率的大幅下行,使得企业的融资成本也快速回落。这一背景下,从5月利率下行开始算起,5~8月美国信用债发行累计同比增长20.6%,投资级债券增长13.7%,高收益债券增长74.5%。

图表:投资和高收益债信用利差分别处于14.6%和32.7%的历史低位

图表:5月到8月,美国投资级债券发行量增长13.7%

图表:高收益级发行大幅增长74.5%

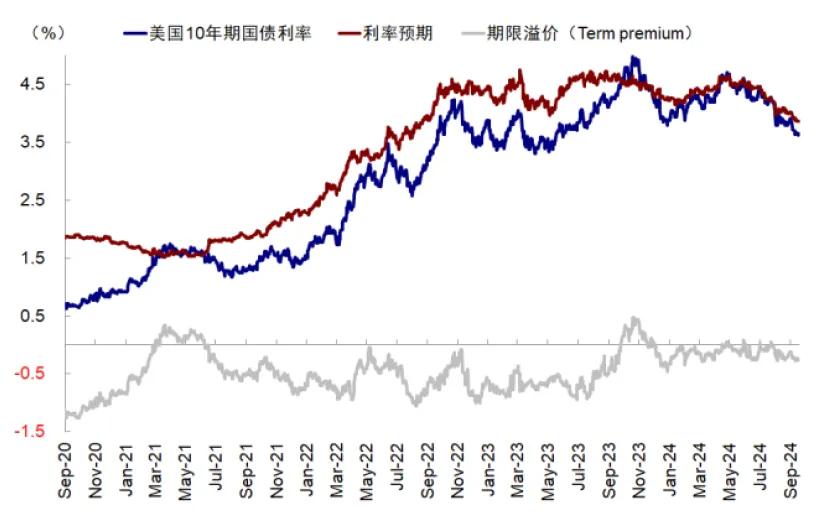

我们静态测算,若货币政策回归中性,10年期美债利率的高点和低点分别为3.8%和3.5%(中性利率1.4%+通胀预期2.1%+期限溢价0-30bp)。

图表:假设r*在1.4%,通胀预期2.1%,期限溢价0-30bp附近,美债在3.5%-3.8%区间

图表:考虑利差压力和金融风险,美联储可能仅共需要降息125-175bp左右

当然,如果为了使当前货币政策摆脱限制性(restrictive)以解决各环节融资成本偏高的问题,其实需要的降息幅度可能更小,目前各环节的融资成本都已经明显下行,尤其是低于投资回报率,体现为上文中提到的 居民的按揭利率、企业信用债利差等。只不过,企业端因为行业的差异会反映的慢一些,同时美联储也可能希望初始以更快的降息来更快的实现这一效果,但并不意味着后续路径会必然如此。目前,上述金融条件的宽松还尚未反映到实际的宏观硬数据上,这既是增长放缓与政策宽松的“青黄不接”,也是这一阶段市场预期混乱和波动的原因。

图表:企业融资成本和投资回报率打平对应10年期美债4.3%

如何交易降息?宽松交易而非衰退交易;分母资产向分子资产逐步切换;短债、地产链和工业金属值得关注;对中国影响看是否能有效传导

从历次降息的一般性的规律看,我们以简单平均方式,总结了90年代以来历轮降息周期中各类资产的表现。一般而言,降息前,分母资产(如美债、黄金、罗素2000和港股生物科技为代表的小盘成长股等)表现较好,分子资产表现不佳(如铜、美股和周期板块等),但降息后待宽松效果逐步显现,分子资产逐渐开始跑赢。

不过,将历史经验简单平均的最大问题是掩盖了每次降息周期的差异。不加区分宏观环境的历史经验对比不仅没有意义、还会造成误导,上文中“平均规律”提到的分母资产向分子资产的切换,究竟是第一次降息后切换,还是第10次降息后才切换,本质上取决于经济放缓的程度所需要匹配的降息次数,而非降息这件事本身,否则完全可能“做反”,例如2019年降息周期中,第一次降息后,美债利率逐步见底,黄金逐步见顶,铜和美股逐步见底反弹,便实现了切换,如果此时继续加仓长端美债和黄金的话,操作上就完全反向了。

图表:历史可比阶段如1995和2019年的三次共75bp降息

目前来看,50bp起步的非常规降息,短期依然会使得市场担心未来的增长是否会面临更大压力,因此未来几个经济数据就至关重要。如果数据不大幅恶化,甚至如我们预期的那样,在一些利率敏感端,如地产等还能有所改善,那么就会给市场传递一个“降息程度够且经济不差”的组合,达到新的平衡,后续市场主线或转向降息后的修复交易。

因此在当前环境,美债和黄金还无法证伪这一预期下,仍可能有一定持有机会但短期空间有限,如果后续数据证实经济压力不大,那么这些资产应该适时退出;相比之下,更为确定的是直接受益于美联储降息的短债、逐步修复的地产链(甚至拉动中国相关出口链)以及铜也逐步关注,但目前仍有些偏左侧,需要等待后续几个数据验证《降息交易的新思路》)。

图表:基于我们的流动性模型测算,美股在四季度之前依然有回撤风险,但不改变降息后周期修复的再配置空间

对于中国市场,观察美联储降息最主要的影响逻辑是外围宽松效果如何传导进来,也即国内政策在这一环境下如何应对。考虑到中美利差与汇率的约束,美联储降息将为国内提供更多的宽松窗口和条件,这也是当前相对较弱的增长环境和依然偏高的融资成本所需要的。因此,我们认为,如果国内宽松力度强于美联储,将给市场带来更大提振。反之,如果幅度有限,也是当前现实约束下更可能的情形,那么美联储降息对中国市场的影响可能就是边际和局部的,2019年降息周期即是如此。

图表:回调反而提供介入降息交易的机会,当前宽松交易过半,再通胀交易还未完成

从这一角度出发,港股因为对外部流动性敏感,以及联系汇率安排下香港跟随降息的缘故,其弹性较A股更大。同理,在行业层面,对利率敏感的成长股(生物科技、科技硬件等)、海外美元融资占比较高的板块、港股本地分红甚至地产等,以及受益于美国降息拉动地产需求的出口链条,也可能会在边际上受益。

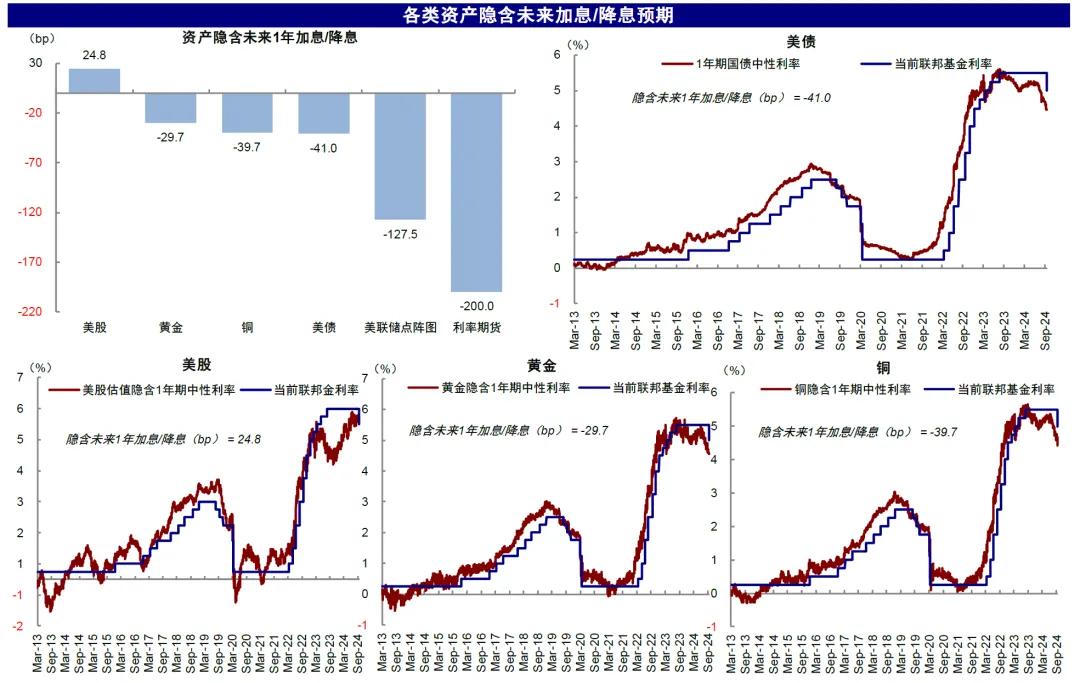

此外,各类资产或在不同程度上“抢跑”降息路径,我们测算,目前计入降息预期多少的程度排序为,利率期货(200bp)>美债(41bp)>铜(40bp)>黄金(30bp)>美股(+25bp),这也是我们建议适度“反着想、反着做”的主要含义。

图表:我们测算,目前利率期货共计入200bp降息,美债、铜和黄金分别计入41、40、30bp降息,美股计入25bp加息

刘刚,CFA 分析员 SAC 执证编号:S0080512030003 SFC CE Ref:AVH867

王子琳 联系人 SAC 执证编号:S0080123090053

杨萱庭 分析员 SAC 执证编号:S0080524070028

李雨婕 分析员 SAC 执证编号:S0080523030005 SFC CE Ref:BRG962■

玉渊谭天丨美联储四年来首次降息意味着什么?

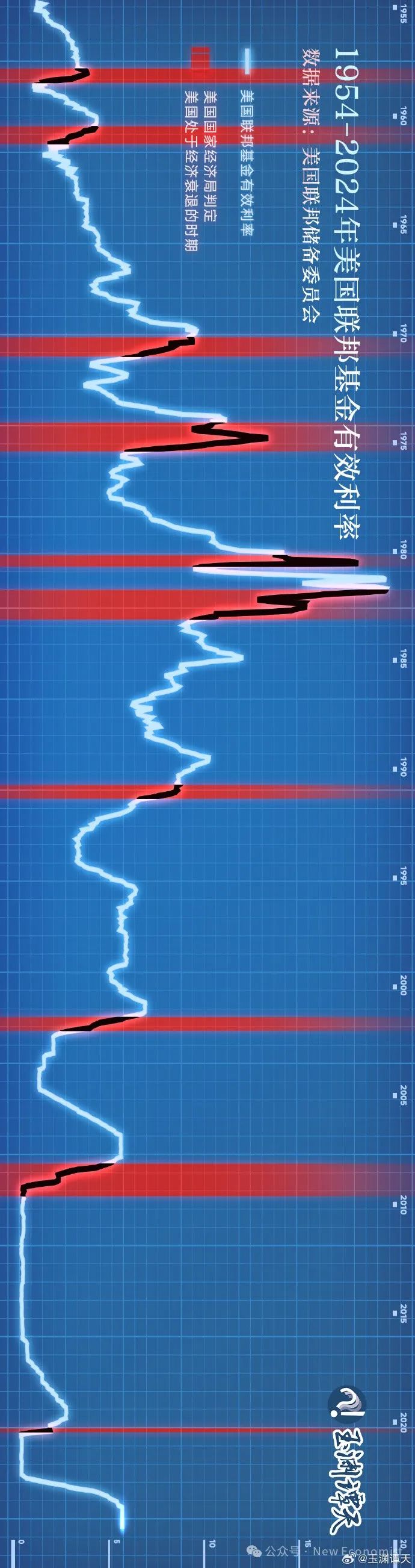

当地时间18日,美联储宣布将基准利率目标范围下调50个基点,降至4.75%~5%,这是自2020年3月以来的首次降息。在这4年间,美联储共加息11次,基准利率从0%~0.25%持续加到5.25%~5.5%。

历史上,几乎每轮降息周期,都伴随着美国经济的衰退。

这张美国有效联邦基金利率(Effective Federal Funds Rate)的图中,红色阴影区域是美国国家经济研究局(National Bureau of Economic Research)判定美国处于经济衰退的时期。

可以看到,从70年代石油危机、80年代储贷危机、世纪之交的互联网泡沫,到2008年全球金融危机和2019年全球新冠疫情,美联储每一次大幅降息,都跟衰退的阴影区间高度重合。

这就是为什么降息有时被视为“经济疲软的信号”——美联储通常在经济出现问题时才会采取降息行动,试图通过更宽松的货币政策来刺激经济复苏。■

特别声明:以上内容仅代表作者本人的观点或立场,不代表新浪财经头条的观点或立场。如因作品内容、版权或其他问题需要与新浪财经头条联系的,请于上述内容发布后的30天内进行。